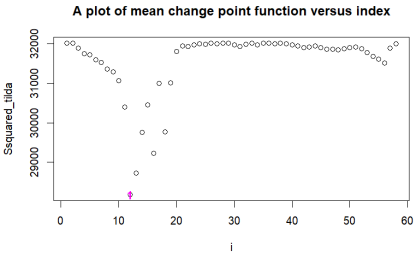

Change-point detection is the point or location in the series where the observations of that series are shifted to another point. Inflation is considered as one of the most important determinants of economic growth and also a key macroeconomic indicator which shows how prices of goods change from one period to another and this plays a critical role in economic stability and growth. The study therefore, aimed to determine structural change-point(s) of the inflation rate in Ghana, which will serve as an essential source of information to guide policy direction. Annual data on Ghana’s inflation rate were sourced from the World Bank website covering the years 1965-2025. To remove the effect of serial correlation since the inflation data was collected over time, an ARIMA model was considered and the errors which were independent and identically distributed, were extracted for multiple change point procedures. Change point methods considered were the Cumulative Sum (CUSUM) Test, the Binary Segmentation (BS) Method and the Pruned Exact Linear Time (PELT) Algorithm. We sought to determine change points in mean, variance (risk) and mean-variance jointly since they are the basic measured quantities for econometric analysis. Results show that the mean change point was detected at time (index) 12, which represents the year 1976, corresponding to Ghana’s mid-1970s macroeconomic instability. Variance (risk) change points were detected at time points 37 and 56, which represent the years 2001 and 2020, respectively corresponding to times of fiscal stress (Ghana joining the Heavily Indebted Poor Countries (HIPC)), electoral spending and COVID-19 shock. The mean-variance change points were also detected at time points 10 and 20, which represent the years 1974 and 1984, respectively aligning with the oil shock era and the economic recovery programme (ERP) regime. The study showed that Ghana’s inflation process has experienced multiple structural shifts associated with major economic shocks and policy transitions. It is highly recommended that credible macroeconomic management and fiscal discipline be adhered to during structural changes.

| Published in | American Journal of Theoretical and Applied Statistics (Volume 15, Issue 2) |

| DOI | 10.11648/j.ajtas.20261502.13 |

| Page(s) | 47-58 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

Inflation, Change Point, CUSUM, Binary Segmentation, Pruned Exact Linear Time

are two distinct values of. Next, let be the shift-position. The main concern of change point detection is to get the values of using the observations .

are two distinct values of. Next, let be the shift-position. The main concern of change point detection is to get the values of using the observations . Statistic | Value |

|---|---|

N | 60 |

Mean | 27.17 |

Median | 18.04 |

Min | -8.42 |

Max | 122.87 |

Std Dev | 26.34 |

Skewness | 2.12 |

Kurtosis | 4.71 |

Test | Test statitic | p-value | Decision |

|---|---|---|---|

ADF | -2.6057 | 0.33 | Non- stationary |

KPSS | 0.3231 | 0.10 | Stationary |

Test | Test statistic | p-value | Decision |

|---|---|---|---|

ADF | -4.8454 | 0.01 | Stationary |

KPSS | 0.048223 | 0.10 | Stationary |

model | AIC | AICc | BIC | log likelihood |

|---|---|---|---|---|

ARIMA (0,1,1) | 559.95 | 560.17 | 564.07 | -277.97 |

ARIMA (0,1,2) | 543.05 | 543.49 | 549.23 | -268.52 |

ARIMA (1,1,1) | 545.59 | 546.04 | 551.78 | -269.80 |

ARIMA (1,1,2) | 551.79 | 552.54 | 560.03 | -271.89 |

ARIMA (2,1,1) | 545.84 | 546.60 | 554.08 | -268.92 |

ARIMA (2,1,2) | 546.48 | 547.63 | 556.78 | -268.24 |

Lag | Statistic | Df | p-value |

|---|---|---|---|

12 | 11.042 | 12 | 0.5253 |

24 | 18.029 | 24 | 0.8016 |

36 | 20.238 | 36 | 0.9841 |

Index | Residuals | Year | Ŝ2 |

|---|---|---|---|

1 | -0.01320687 | 1965 | 32015.53 |

2 | -4.29354509 | 1966 | 32010.31 |

3 | 21.7550011 | 1967 | 31888.66 |

4 | 11.9035086 | 1968 | 31750.44 |

5 | 4.47419253 | 1969 | 31725.37 |

6 | 10.5231692 | 1970 | 31597.09 |

7 | 7.06457307 | 1971 | 31523.77 |

8 | 11.4883496 | 1972 | 31364.51 |

9 | 6.4308659 | 1973 | 31296.52 |

10 | 14.0655877 | 1974 | 31069.34 |

11 | 30.994677 | 1975 | 30401.88 |

12 | 70.752934 | 1976 | 28181.17 |

13 | -9.38544771 | 1977 | 28726.15 |

14 | -28.057991 | 1978 | 29763.88 |

15 | -23.5398904 | 1979 | 30456.93 |

16 | 47.6274934 | 1980 | 29230.91 |

17 | -69.7493222 | 1981 | 30997.97 |

18 | 55.9577423 | 1982 | 29773.68 |

19 | -54.1725452 | 1983 | 31010.06 |

20 | -61.5940094 | 1984 | 31805.29 |

21 | -22.0057488 | 1985 | 31943.48 |

22 | 1.45027606 | 1986 | 31935.66 |

23 | -8.58315793 | 1987 | 31970.57 |

24 | -11.7811193 | 1988 | 32002.15 |

25 | 4.3863553 | 1989 | 31991.13 |

26 | -17.1676432 | 1990 | 32015.46 |

27 | -18.0286912 | 1991 | 31999.82 |

28 | 4.18581495 | 1992 | 32008.18 |

29 | 1.99389509 | 1993 | 32011.39 |

30 | 34.757801 | 1994 | 31965.54 |

Index | Residuals | Year | Ŝ2 |

|---|---|---|---|

31 | 6.2326934 | 1995 | 31937.31 |

32 | -15.7456591 | 1996 | 31991.76 |

33 | -22.7265114 | 1997 | 32014.98 |

34 | -22.9702488 | 1998 | 31969.29 |

35 | 21.6010058 | 1999 | 32014.80 |

36 | 13.2120864 | 2000 | 32008.70 |

37 | -24.6623142 | 2001 | 32001.27 |

38 | 5.75038018 | 2002 | 32011.21 |

39 | -8.58841342 | 2003 | 31996.57 |

40 | -7.71257973 | 2004 | 31974.27 |

41 | -8.2701851 | 2005 | 31939.6 |

42 | -5.72710595 | 2006 | 31908.27 |

43 | 2.41206491 | 2007 | 31921.65 |

44 | 4.09622117 | 2008 | 31943.12 |

45 | -6.10527932 | 2009 | 31906.95 |

46 | -5.48734308 | 2010 | 31865.32 |

47 | -0.66976581 | 2011 | 31855.08 |

48 | 0.15616001 | 2012 | 31850.04 |

49 | 3.93799895 | 2013 | 31876.19 |

50 | 3.94575075 | 2014 | 31901.09 |

51 | 2.57563303 | 2015 | 31914.42 |

52 | -3.56861224 | 2016 | 31874.56 |

53 | -6.57419788 | 2017 | 31781.09 |

54 | -4.39945451 | 2018 | 31675.87 |

55 | 0.26761792 | 2019 | 31615.24 |

56 | 0.32953637 | 2020 | 31514.23 |

57 | 21.3671721 | 2021 | 31884.98 |

58 | 19.085373 | 2022 | 32001.77 |

59 | -4.23925233 | 2023 | - |

Change point location (s) | Years | -2loglike lihood | -2loglike lihood +pen |

|---|---|---|---|

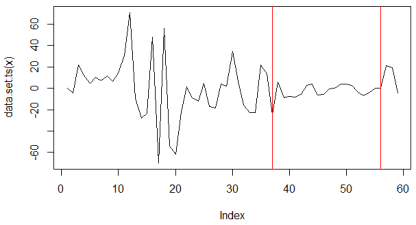

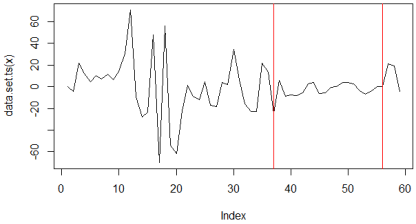

37 | 2001 | 492.8971 | 512.7837 |

56 | 2020 |

Change point location (s) | Years | -2loglike lihood | -2loglike lihood +pen |

|---|---|---|---|

37 | 2001 | 492.8971 | 512.7837 |

56 | 2020 |

Change point location (s) | Years | -2loglike lihood | -2loglike lihood +pen |

|---|---|---|---|

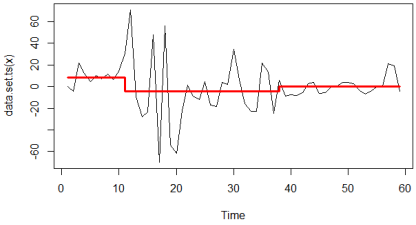

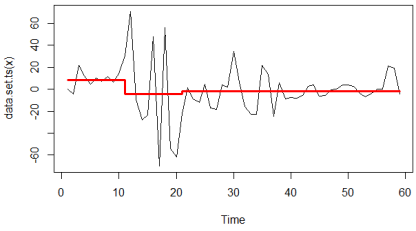

10 | 1974 | 484.7160 | 509.7156 |

37 | 2001 |

Change point location (s) | Years | -2loglike lihood | -2loglike lihood +pen |

|---|---|---|---|

10 | 1974 | 482.6993 | 507.2781 |

20 | 1984 |

ARIMA | Autoregressive Integrated Moving Average Model |

BS | Binary Segmentation (BS) |

CUSUM | Cumulative Sum |

CPD | Change-Point Detection |

ERP | Economic Recovery Programme |

EWMA | Exponentially Weighted Moving Average |

HIPC | Heavily Indebted Poor Countries |

PELT | Pruned Exact Linear Time |

| [1] | Moskvino, V., Zhigljavsky, A. An Algorithm base on Singular Spectrum Analysis for change point Detection. Communications in Statistics- Simulation and Computation. 2023, 32, 319-352. |

| [2] | Chen, J., Gupta, A. K. Parametric Statistical Change Point Analysis: with Applications to Genetics, Medicine, and Finance. Birkhauser, Boston; (2012). |

| [3] | Aminikhanghahi, S., Cook, D. J. A Survey of Methods for Time Series Change Point Detection. Knowledge and Information Systems. 2017, 51(2): 339-367. |

| [4] | Alves, C. C. The Mixed CUSUM- EWMA (MCE) Control Chart. As A New Alternative in the Monitoring of a Manufacturing Process. Brazilian Journal of Operations and Production Management. 2017, 16, 1. |

| [5] | Howard, M. Z. Inflation and performance of listed firms in Ghana. University of Cape Coast, Ghana. (2022). |

| [6] | Mishkin, F. S. The Economics of Money, Banking and Financial markets. (7th ed.). Boston: Pearson/Addison-Wesley; 2004. |

| [7] | Ackley, G. Macroeconomic Theory. New Delhi: Kalyani Publishers; 2008. |

| [8] | Junttila, J. Structural Breaks, ARIMA Model and Finnish Inflation Forecasts. International Journal of Forecasting. 2001, 17, 2, 203-230. |

| [9] | Adu, G., Marbuah, G. Determination of Inflation. An Empirical Investigation. South Africa Journal of Economics. 2011, 79, 3, 251-269. |

| [10] | Alagidede, P., Coleman, S., Cuestas, J. C. Inflation persistence in Ghana: Evidence from Disaggregated Consumer Price Inflation. Economic Modelling. 2011, 36, 413–422. |

| [11] | Czitrom, V. Introduction to Statistical Process Control. Statistical Case Studies for Industrial Process Improvement. 1997, 299-314. |

| [12] | Killick, R., Eckley, I. A. Changepoint: An R Package for Changepoint Analysis. Journal of Statistical Software. 2014, 58, 1-19. |

| [13] | Hutchful, E. Ghana’s Adjustment Experience: The Paradox of Reform. Oxford: James Currey. 2002. |

| [14] | Devereux, M. B., Engel, C. Monetary Policy in the Open Economy Revisited: Price Setting and Exchange-Rate Flexibility. The Review of Economic Studies. 2017, 70, 765-783. |

| [15] | IMF, World Bank. Poverty Reduction Strategy Papers-Progress in implementation. Washington DC. 2002. |

| [16] | Osei, R. D., Quartey, P. Tax Reforms in Ghana (No. 2005/66). WIDER Research Paper. 2005. |

| [17] | Ling, J. Economic Consequences of the COVID-19 Outbreak: The Need for Epidemic Preparedness. Frontiers in Public Health. 2020, 1-19. |

| [18] |

World Bank. Ghana Economic Update. Available from:

https://documents1.worldbank.org/curated/en/099625006292235762/pdf/P177994040f93403091ea0857af510b164.pdf (accessed 3rd February, 2026) |

| [19] | Aryeetey, E., Harrigan, J., Nissanke, M. Economic Reforms in Ghana: The Miracle and the Mirage. Africa World Press. 2000. |

| [20] | Davis, J. Institutional Impediment to Work Force Retrenchments and Restructuring in Ghana’s State Enterprises. World Development. 1991, 19(8), 987-1005. |

| [21] | Andrews, D. W. K. Tests for Parameter Instability and Structural Change with Unknown Change Point. Econometrica. 1993, 61(4), 821. |

APA Style

Zakaria, I., Engmann, G. M., Puurbalanta, R., Osei-Mainoo, A. (2026). Change-Point Detection with ARIMA of Inflation Rate in Ghana. American Journal of Theoretical and Applied Statistics, 15(2), 47-58. https://doi.org/10.11648/j.ajtas.20261502.13

ACS Style

Zakaria, I.; Engmann, G. M.; Puurbalanta, R.; Osei-Mainoo, A. Change-Point Detection with ARIMA of Inflation Rate in Ghana. Am. J. Theor. Appl. Stat. 2026, 15(2), 47-58. doi: 10.11648/j.ajtas.20261502.13

@article{10.11648/j.ajtas.20261502.13,

author = {Issah Zakaria and Gideon Mensah Engmann and Richard Puurbalanta and Angela Osei-Mainoo},

title = {Change-Point Detection with ARIMA of Inflation Rate in Ghana},

journal = {American Journal of Theoretical and Applied Statistics},

volume = {15},

number = {2},

pages = {47-58},

doi = {10.11648/j.ajtas.20261502.13},

url = {https://doi.org/10.11648/j.ajtas.20261502.13},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ajtas.20261502.13},

abstract = {Change-point detection is the point or location in the series where the observations of that series are shifted to another point. Inflation is considered as one of the most important determinants of economic growth and also a key macroeconomic indicator which shows how prices of goods change from one period to another and this plays a critical role in economic stability and growth. The study therefore, aimed to determine structural change-point(s) of the inflation rate in Ghana, which will serve as an essential source of information to guide policy direction. Annual data on Ghana’s inflation rate were sourced from the World Bank website covering the years 1965-2025. To remove the effect of serial correlation since the inflation data was collected over time, an ARIMA model was considered and the errors which were independent and identically distributed, were extracted for multiple change point procedures. Change point methods considered were the Cumulative Sum (CUSUM) Test, the Binary Segmentation (BS) Method and the Pruned Exact Linear Time (PELT) Algorithm. We sought to determine change points in mean, variance (risk) and mean-variance jointly since they are the basic measured quantities for econometric analysis. Results show that the mean change point was detected at time (index) 12, which represents the year 1976, corresponding to Ghana’s mid-1970s macroeconomic instability. Variance (risk) change points were detected at time points 37 and 56, which represent the years 2001 and 2020, respectively corresponding to times of fiscal stress (Ghana joining the Heavily Indebted Poor Countries (HIPC)), electoral spending and COVID-19 shock. The mean-variance change points were also detected at time points 10 and 20, which represent the years 1974 and 1984, respectively aligning with the oil shock era and the economic recovery programme (ERP) regime. The study showed that Ghana’s inflation process has experienced multiple structural shifts associated with major economic shocks and policy transitions. It is highly recommended that credible macroeconomic management and fiscal discipline be adhered to during structural changes.},

year = {2026}

}

TY - JOUR T1 - Change-Point Detection with ARIMA of Inflation Rate in Ghana AU - Issah Zakaria AU - Gideon Mensah Engmann AU - Richard Puurbalanta AU - Angela Osei-Mainoo Y1 - 2026/04/15 PY - 2026 N1 - https://doi.org/10.11648/j.ajtas.20261502.13 DO - 10.11648/j.ajtas.20261502.13 T2 - American Journal of Theoretical and Applied Statistics JF - American Journal of Theoretical and Applied Statistics JO - American Journal of Theoretical and Applied Statistics SP - 47 EP - 58 PB - Science Publishing Group SN - 2326-9006 UR - https://doi.org/10.11648/j.ajtas.20261502.13 AB - Change-point detection is the point or location in the series where the observations of that series are shifted to another point. Inflation is considered as one of the most important determinants of economic growth and also a key macroeconomic indicator which shows how prices of goods change from one period to another and this plays a critical role in economic stability and growth. The study therefore, aimed to determine structural change-point(s) of the inflation rate in Ghana, which will serve as an essential source of information to guide policy direction. Annual data on Ghana’s inflation rate were sourced from the World Bank website covering the years 1965-2025. To remove the effect of serial correlation since the inflation data was collected over time, an ARIMA model was considered and the errors which were independent and identically distributed, were extracted for multiple change point procedures. Change point methods considered were the Cumulative Sum (CUSUM) Test, the Binary Segmentation (BS) Method and the Pruned Exact Linear Time (PELT) Algorithm. We sought to determine change points in mean, variance (risk) and mean-variance jointly since they are the basic measured quantities for econometric analysis. Results show that the mean change point was detected at time (index) 12, which represents the year 1976, corresponding to Ghana’s mid-1970s macroeconomic instability. Variance (risk) change points were detected at time points 37 and 56, which represent the years 2001 and 2020, respectively corresponding to times of fiscal stress (Ghana joining the Heavily Indebted Poor Countries (HIPC)), electoral spending and COVID-19 shock. The mean-variance change points were also detected at time points 10 and 20, which represent the years 1974 and 1984, respectively aligning with the oil shock era and the economic recovery programme (ERP) regime. The study showed that Ghana’s inflation process has experienced multiple structural shifts associated with major economic shocks and policy transitions. It is highly recommended that credible macroeconomic management and fiscal discipline be adhered to during structural changes. VL - 15 IS - 2 ER -

Department of Statistics and Actuarial Science, University of Technology and Applied Sciences, Navrongo, Ghana

Biography: Issah Zakaria is a Mathematics tutor at Ahafoman Senior High Technical School, Goaso, Ghana. He completed his Master of Philosophy degree in Statistics at the University of Technology and Applied Sciences, Navrongo, Ghana in 2024 and his first degree in Statistics at the University for Development Studies, Ghana in 2013. He is currently pursuing his PhD in Statistics at the University of Technology and Applied Sciences, Navrongo, Ghana.

Department of Biometry, University of Technology and Applied Sciences, Navrongo, Ghana

Biography: Gideon Mensah Engmann obtained his Master’s degree in Statistics (Biostatistics) in 2009 from the Center for Statistics, University of Hasselt, Belgium. He earned his PhD in Statistics from the School of Mathematical Sciences, Shanghai Jiao Tong University, People’s Republic of China in 2021. He is a Senior Lecturer at the Department of Biometry, University of Technology and Applied Sciences, Navrongo, Ghana. His current research interest includes Statistical Process Control and its Applications.

Department of Statistics and Actuarial Science, University of Technology and Applied Sciences, Navrongo, Ghana

Biography: Richard Puurbalanta earned his PhD in Statistics from the University for Development Studies, Ghana. He is a Senior Lecturer at the Department of Statistics and Actuarial Science, University of Technology and Applied Sciences, Navrongo, Ghana. His current research interest includes Spatial and Bayesian Statistics.

Department of Statistics and Actuarial Science, University of Technology and Applied Sciences, Navrongo, Ghana

Biography: Angela Osei-Mainoo is an Assistant Lecturer at the Department of Statistics and Actuarial Science, University of Technology and Applied Sciences, Navrongo, Ghana. She completed her MPhil. in Applied Mathematics (Statistics) in 2013 and is currently a PhD candidate at Kwame Nkrumah University of Science and Technology, Ghana where she attained both her first and second degrees.

Figure 1. ACF and PACF plot of inflation rate.

Figure 2. ACF and PACF plot of first difference of inflation rate.

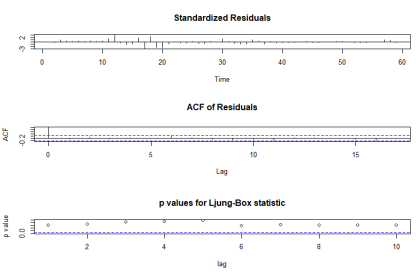

Figure 3. Model diagnosis of ARIMA (0, 1, 2).

Figure 4. Mean Change Detection of Inflation Rate in Ghana.

Figure 5. Variance change point detection by binary segmentation.

Figure 6. Variance change point detection by pelt algorithm.

Figure 7. Mean-variance change point detection by Binary Segmentation.

Figure 8. Mean-variance change points detection by PELT method.

Information