Abstract

This study investigates the role of financial literacy as a key driver of financial inclusion and behavioral empowerment among Ukrainian youth in the context of digital transformation and post-crisis economic recovery. Based on a large-scale survey of 948 respondents aged 18–25, the research employs an integrated methodological framework that combines index modeling, correlation analysis, and multivariate linear regression. Financial literacy is operationalized through a composite index constructed in accordance with the OECD/INFE methodology, incorporating financial knowledge, financial behavior, and financial attitudes. The results indicate a moderate overall level of financial literacy among Ukrainian youth, with an average index value of 0.591 on a normalized scale of 0–1. While theoretical financial knowledge demonstrates relatively stronger performance, practical financial behavior and attitudinal confidence remain comparatively weaker, revealing a persistent behavioral gap between awareness and action. Correlation analysis confirms strong internal consistency within the knowledge and behavior components, but only limited spillover from knowledge to real financial practices. Regression estimates reveal that self-confidence in personal financial knowledge is the only statistically significant predictor of financial inclusion (β = 0.0529, p < 0.01), whereas age, formal education, budgeting horizon, and financial independence exhibit no robust explanatory power. This finding highlights the decisive role of psychological factors in shaping financial behavior beyond formal human capital characteristics. The findings confirm that financial literacy influences financial inclusion not primarily through formal knowledge or education, but through psychological confidence and subjective financial capability. Access to financial services alone is insufficient without behavioral readiness and autonomy in decision-making. The study provides empirical evidence that confidence-oriented financial education, combined with digital financial infrastructure, is crucial for promoting sustainable financial inclusion among young people. These findings carry important implications for public policy in post-war and transition economies, emphasizing the need for integrated national strategies that link education, digitalization, and behavioral empowerment.

Keywords

Financial Literacy, Financial Inclusion, Financial Behavior, Index Modeling, Economic Empowerment, Financial Capability

1. Introduction

Global economic shocks to the existing world balance and digital transformation pose new challenges for scientists and practitioners. In such conditions, financial literacy is seen not only as an individual competence, but as a key indicator of the socio-economic stability of the population. The general awareness of the population in financial matters is a crucial tool for making informed financial decisions, which will form the basis for the population's financial stability during times of turbulence and crisis. Developing financial literacy ensures sound economic decisions and effective management of personal finances, and increases adaptability to changes in the financial environment. Some scholars, such as Iryna Bilous, link the financial literacy of the population to factors ensuring financial security at both the household and state levels

.

The relevance of this study lies in the fact that, despite numerous government and international initiatives, the level of financial literacy among young people remains uneven, and financial inclusion remains selective, particularly among vulnerable social groups.

Studies conducted by the OECD in 2020, the World Bank, and the G20 demonstrate a close link between financial literacy and access to formal financial instruments

.

The concept of financial literacy in contemporary literature is defined as a combination of knowledge, skills, attitudes, and behavioral patterns that enable an individual to make informed financial decisions and achieve financial well-being

. Thus, the OECD defines financial literacy as a combination of awareness, knowledge, skill, attitude, and behavior necessary to make sound financial decisions and achieve financial well-being. This definition emphasizes complexity, behavior, and well-being as the main elements of financial literacy. At the same time, the G20 emphasizes the life cycle orientation and focuses on practical management.

The Central Bank of Ukraine considers financial literacy to be a person's ability to make responsible decisions regarding the management of their own funds, bringing responsibility and awareness to the forefront of decision-making

.

At the same time, international publications emphasize the link between literacy and the ability to manage resources throughout the entire life cycle

| [6] | Mandal, B. K., Kumari, S., & Das, P. Impact of government-led saving initiative on women empowerment and financial inclusion in rural population: evidence from Amar Bari Amar Khamar (ABK) project in Bangladesh, Lex localis-journal of local self-governmen, Vol. 23, NS3 (2025)

https://lex-localis.org/index.php/LexLocalis/article/view/800643/1415 |

[6]

. At the same time, special attention is paid to young people as a key demographic group that needs not only knowledge, but also motivation and digital skills for financial integration

| [7] | Prihatiningsih, P., & Pradana, M. R. A. Gen Z crypto investment: The role of FOMO, influencer, return, and financial literacy, Indonesian Journal of Banking and Financial Technology. 2025. https://doi.org/10.55927/fintech.v3i4.110 |

[7]

.

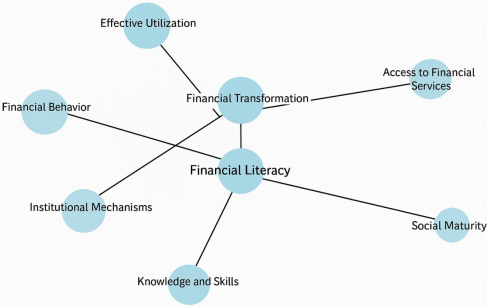

Financial literacy and financial inclusion are interrelated components of modern socio-economic policy. Most authors interpret financial literacy not only as a sum of knowledge and skills, but also as an integral characteristic of a personality that is shaped by social values, behavioral attitudes, and digital competencies. At the same time, financial inclusion is increasingly seen not as passive access to services, but as the active participation of different social groups in the financial system, provided there is sufficient awareness and institutional support.

Modern approaches involve combining educational policy with digital platforms and social engagement, thereby forming a comprehensive ecosystem for sustainable financial development.

The relationship between financial inclusion and financial literacy is shown in

Figure 1.

Figure 1. The Link Between Financial Literacy and Financial Inclusion.

In the context of the digital economy, financial literacy is closely linked to expanding opportunities for participation in the financial system, which is defined as financial inclusion. According to the World Bank, financial inclusion encompasses not only access to accounts but also the ability to safely, effectively, and efficiently utilize a wide range of financial services

| [9] | World Bank. Financial Inclusion. Financial inclusion is a key enabler to reducing poverty and boosting prosperity. |

[9]

. Financial inclusion is a catalyst for achieving seven of the 17 Sustainable Development Goals (SDGs)

. It fosters economic growth and employment, promotes economic empowerment of women, and contributes to eliminating poverty.

The works of Nila Tri Setiawati and Rasistia Wisandianing Primadineska examine how literacy influences investment readiness, savings, and the use of financial technologies, particularly among Generation Z

| [11] | Setiawati, N. T. and Primadineska, R. W. Financial Behavior of Generation Z in Indonesia: Impact of Literacy, Technology and Lifestyle, Telaah Bisnis. 2025, 2 6, 55-68.

https://doi.org/10.35917/tb.v26i1.596 |

[11]

.

Ukrainian researchers are rethinking both concepts in the national context. Tkachuk, Yevtushenko, and Stetsenko interpret financial literacy as an integral characteristic that encompasses educational, behavioral, and digital components

| [12] | Tkachuk, N., Novosad, O. Formation of the key competence “entrepreneurship and financial literacy” in the educational process in geography, Scientific Notes of Vinnytsia State Pedagogical University named after Mykhailo Kotsyubinsky. Series: Theory and Methods of Teaching Natural Sciences. 2024, 7, 22-31.

https://doi.org/10.31652/2786-5754-2024-7-22-31 |

| [13] | Yevtushenko, N., Stetsenko, D. Financial Inclusion in Ukraine: Current Status and Prospects for Development, Grail of Science. 18 Jun. 2024, 40, 136-140.

https://doi.org/10.36074/grail-of-science.07.06.2024.015 |

[12, 13]

. Publications by contemporary scholars also emphasize the importance of financial education as a tool for ensuring inclusion.

Krupka, Zamaslo, and others link the level of financial inclusion to the financial stability of local communities. It is also worth noting the growing interest in financial technologies as drivers of inclusion

| [14] | Krupka, M., Zamaslo, O., Petyk, M., Diuh, I. Financial Sustainability of Local Budgets in Ukraine in the Context of Financial Inclusion and Post-War Economic Recovery, World of Finance. 2025, 3(84), 08-23.

https://doi.org/10.35774/sf2025.03.008 |

[14]

.

According to Vidati

| [15] | Vidiati, C., Nursindi, M. The Role of Digital Islamic Economics in Increasing Financial Inclusion in the Fintech Era, Advances in Social Humanities Research. 2024, 2(12), 2279-2289. |

[15]

, fintech — including digital wallets, mobile platforms, and cryptocurrency services —is driving financial participation among young people in developing countries. Similar trends have been observed among Ukrainian youth, with digital platforms increasingly replacing traditional banks, especially in the context of war and migration.

Thus, the available array of scientific sources allows us to conclude that financial literacy is considered a structural element of financial inclusion, as well as a prerequisite for economic self-sufficiency, digital adaptation, and reduction of social inequality. At the same time, the complex dimension of this relationship among Ukrainian youth in the context of post-crisis transformation remains insufficiently researched. At the same time, both the OECD and local authorities in each country are actively engaged in issues related to the relevant assessment of financial literacy levels. Currently, the most widely used methodology is that employed by the OECD. The widespread use of the OECD methodology does not preclude the possibility of scientific research into other measurement methods that would provide more detailed results, aggregated assessments, and identify vulnerabilities that require special attention from regulators and the education system.

Thus, we can define the purpose of this study as an empirical assessment of the level of financial literacy among young people in Ukraine and an analysis of its impact on their ability to use financial products and services, taking into account variables such as knowledge, financial behavior (demonstrating moderate application of knowledge), and financial attitudes (awareness of the need for knowledge, independence, education). Comparison of the results obtained with those of similar studies in Ukraine from previous years to establish the dynamics of change. Comparison of the results of the empirical research with those of other countries. Assessment of changes in individual components to identify promising areas of potential impact. Identification of areas of practical implications for further growth in financial literacy and ensuring financial inclusion.

To achieve this goal, a questionnaire survey was conducted among 948 respondents aged 18-27, and index modeling, correlation analysis, and linear regression modeling tools were applied.

The study’s results enabled the assessment of the current level of financial literacy among young people using the OECD methodology, the identification of thematic sub-indices, and the establishment of a statistically significant relationship between awareness levels and financial inclusion.

The results of the survey were evaluated using the OECD methodology and compared with previous studies that measured financial literacy in Ukraine during the pre-war period. A trajectory of improvement in financial literacy was identified, and its positive impact on financial inclusion in Ukraine was established, despite the challenging economic and digital landscape. The findings are important for the development of targeted educational programs, state financial strategy, and digital inclusion policies in Ukraine.

2. Materials and Methods

To solve the tasks set, the author used an online survey among Ukrainian youth aged 18-25. A total of 948 respondents took part in the survey, which we consider sufficient for quantitative empirical research. The primary characteristics of the survey method, including standardization, mass participation, and representativeness, enabled the statistical processing of the results.

Within the framework of this empirical study, a questionnaire method was employed—a standardized quantitative approach for collecting primary sociological data.

The methodological basis was a structured questionnaire containing both closed-ended and semi-open-ended questions, aimed at identifying the level of financial literacy among young people. The questionnaire included both closed and semi-open questions covering knowledge of basic financial concepts, awareness of economic processes (inflation, devaluation, investment), as well as aspects of personal financial behavior (budget planning, degree of financial independence, choice of savings methods).

The survey allowed us to:

1) collect quantifiable data on respondents' knowledge, attitudes, and behavior in the financial sphere;

2) ensure consistency of survey information through a standardized set of questions;

3) conduct further statistical analysis (calculation of proportions, construction of indices, average values, etc.).

The study is empirical in nature, based on respondents' self-assessments and actual behavioral habits. The sample was formed based on accessibility and voluntary participation, and the survey was conducted online using Google Forms. The survey was conducted online using Google Forms from May to October 2025. Participants were aged 18-25, university students and graduates, who are one of the key age groups in terms of financial awareness development. A total of 948 valid responses were received and used for further analysis. The sample was formed using non-probability convenience sampling, which, despite limitations on generalization, allows for obtaining basic guidelines for diagnosing the problem.

A structured questionnaire containing both closed and semi-open questions was used as a data collection tool. The wording of the questions was adapted in accordance with the OECD/INFE recommendations for assessing the financial literacy of the adult population, which ensures consistency with international approaches and comparability of data

.

The validity of the questionnaire is ensured using standardized wording in accordance with the OECD/INFE international methodology and coverage of all three recommended components of financial literacy: knowledge, financial behavior, and attitudes. The coverage of the large sample (n = 948) is equivalent to the typical minimum of 1,000 people used in the OECD international survey. To ensure the validity of the tool, a pilot test of the questionnaire was conducted on a separate group of students (n = 10), after which the wording of some questions was refined.

Conceptual validity is ensured by covering all the main components of financial literacy, including knowledge, skills, and attitudes. In terms of reliability, the uniformity of questions, the standardization of response formats, and the absence of external influences during the survey contributed to the stability of the results.

The standardized format of the questions confirms the reliability of the study, the consistency of the scales, and the clarity of the answer options, as well as the use of quantitative indicators to form an integrated indicator and thematic sub-indices. These characteristics of the method allow us to consider the results obtained as highly reliable within the studied group — young Ukrainian students.

The collected data was exported to.csv format and processed using the Python software environment. First, the array was cleaned of empty and technical records. For quantitative analysis, variables were formed based on binary coding of responses: each respondent was assigned a value of 1 or 0 depending on whether they gave an answer indicating the presence of relevant financial competence. In total, nine such indicators were identified, including knowledge of what a mortgage is, understanding of the consequences of inflation and devaluation, awareness of the concept of a CVV code, ability to plan a budget, independence in making financial decisions, and attitudes towards financial matters.

Based on these variables, an integral indicator of financial literacy for each respondent was calculated as the arithmetic mean of all nine criteria. For a more in-depth analysis, these criteria were grouped into two sub-indices: the first covered basic financial knowledge, and the second covered behavioral skills. This approach allows not only to assess the overall level of literacy, but also to identify disparities between theoretical knowledge and practical skills in applying it in everyday life.

To assess the level of financial literacy among young people, an approach developed by the Organization for Economic Cooperation and Development (OECD) was used, which involves multidimensional measurement of financial literacy in three key areas: financial knowledge, financial behavior, and financial attitudes

.

The integrated financial literacy index was calculated based on the methodology developed by the Organisation for Economic Co-operation and Development (OECD), which emphasizes a multidimensional measurement approach. This framework assesses individual financial competence across three key domains: financial knowledge, financial behavior, and financial attitudes. For each respondent, individual indices were computed as follows:

Financial Knowledge Index (K) – calculated as the average score of correct responses to questions assessing understanding of key financial and economic concepts such as inflation, devaluation, CVV codes, mortgage definition, war bonds, pension systems, and the distinction between saving and investing.

Financial Behavior Index (B) – calculated from answers related to practical financial habits, such as budget planning, preferred methods of saving, savings currency, and compliance with tax obligations (e.g., payment of the military levy).

Financial Attitude Index (A) – based on self-reported attitudes, including perceived lack of financial knowledge, financial independence from others (e.g., parents), and possession of higher education. The Materials and Methods section should provide comprehensive details to enable other researchers to replicate the study and further expand upon the published results. If you have multiple methods, consider using subsections with appropriate headings to enhance clarity and organization.

All variables were coded on a binary scale (1 = literate/positive/informed response, 0 = non-literate/neutral/negative response). After computing the individual component scores, an overall financial literacy score was obtained by calculating the unweighted arithmetic mean of the three dimensions:

OECD FinLit Indexᵢ = (Kᵢ + Bᵢ + Aᵢ) / 3(1)

Where:

Kᵢ – Financial Knowledge Index for respondent i

Bᵢ – Financial Behavior Index

Aᵢ – Financial Attitudes Index.

The resulting integrated index (OECD FinLit Index) ranges from 0 to 1, with higher values indicating stronger overall financial literacy. For aggregate analysis, the mean value of the index was calculated across all respondents in the sample.

To determine the overall level of financial literacy, an integrated index was constructed, calculated as the arithmetic mean of nine binarized indicators that cover both knowledge of basic financial concepts (inflation, mortgages, investments) and behavioral characteristics (budget planning, financial independence, confidence in decision-making).

Correlation analysis, using Pearson's coefficient calculation, was employed to examine the internal relationships between variables. The relationships were visualized using a correlation matrix (heatmap).

In addition, to determine the impact of individual socio-demographic factors (age, education, degree of financial independence, budgeting horizon, self-assessment of knowledge) on the level of financial literacy, a multivariate linear regression model was constructed using the least squares method (OLS). The dependent variable was an integral indicator, while the independent variables were standardized numerical and categorical predictors. The model enabled the identification of key determinants of financial literacy and their assessment of significance in explaining interpersonal variation.

3. Results

3.1. Assessment of Financial Literacy Based on the Calculation of the Financial Literacy Index

The study analyzed the responses of an online survey of 948 respondents aged 18-25. To assess the financial literacy of young people in Ukraine, we used a methodology that measures financial literacy across three main areas, the weight and significance of which are shown in

Table 1.

Table 1. How Does the OECD/INFE Assess the Level of Financial Literacy.

Component | Max score | Essence |

Knowledge | 7 | Theoretical knowledge: inflation, compound interest, risk, etc. |

Behaviour | 9 | Budgeting, saving, comparing prices, choosing products |

Attitudes | 5 | Attitude towards money, long-term decisions |

Based on the above components, the authors calculated the financial literacy index using the following formula (

1): the elements of the formula are described in the research methodology.

As a result of the calculations, we have an average index of 59.1% among 948 young people surveyed in Ukraine. This means that, on average, young people possess less than 60% of the key financial knowledge, skills, and attitudes considered essential for effective personal financial management. This result (59.1) is the lower level "average" financial literacy, according to the OECD/INFE 2023 international methodology. The result corresponds to the threshold average level of financial literacy according to OECD criteria, where the average score in most countries ranges between 55% and 70%.

Basic knowledge made the highest contribution, but practical financial actions and confidence in decision-making remain weak.

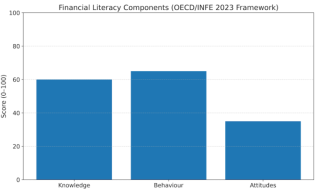

Figure 1 is the visual breakdown of financial literacy among Ukrainian youth based on the OECD/INFE 2023 framework scaled to 100 points:

1) Financial Knowledge Index: ~60.5%

2) Financial Behavior Index: ~59.9%

3) Financial Attitudes Index: ~56.3%.

Figure 2. Financial Literacy Components Built by the Authors.

The graph clearly indicates that all three components are at a moderate level, with none of the dimensions reaching a high proficiency level.

Let us track the dynamics of changes in financial literacy in Ukraine. To achieve this, we will compare the overall financial literacy index, as per the OECD methodology, for Ukraine, which stood at 12.3 points (or 58% of its maximum value) in 2021. The results are presented in

Table 2.

Table 2. Dynamics of Changes in Financial Literacy in Ukraine for the Period 2020-2025.

Year | Source | % of maximum | Comments |

2020 | OECD/INF | ≈57.1% | Data from the OECD regional review |

2021 | NBU /USAID / OECD | ≈57.6% | National survey of the adult population |

2025 | our survey of young people | 59.1% | Budgeting, saving, comparing prices, choosing products |

The financial literacy index in Ukraine is currently showing good dynamics – in less than three years, there has been a 2.0% increase in points; all components of the index have improved. Our research indicates an increase in financial literacy compared to 2021, the last year before Russia's large-scale invasion began. The aggression on the part of the Russian Federation has completely changed the landscape of financial services markets and the educational process in the country. However, even in a situation of uncertainty and powerful external shocks, the results of our study allow us to assert that there is a positive trend in the level of financial literacy among young people in Ukraine.

For a deeper understanding of the significance of the result obtained and to assess the relevance of the financial literacy index value obtained, it is advisable to compare it with the level of financial literacy measured using the same principle in other countries. The comparison with other countries is presented in

Table 3.

Table 3. Comparison of financial literacy levels in Ukraine and other countries around the world, 2023.

Country | Total out of 100 |

Chili | 56.3% |

Portugal | 61.9% |

Italy | 53.1% |

Croatia | 62.0% |

Thailand | 71.7% |

Brazil | 60.6% |

Lithuania | 56,0% |

Ukraine | 59.1% (2025) |

Ukraine’s youth financial literacy score (59.1%) is close to the OECD average (61.9%), slightly lower than Portugal or Thailand, and similar to Croatia or Brazil. This suggests that Ukrainian youth are not significantly behind their global peers but still have room for growth — especially in financial attitudes.

A comparison of the results obtained by the authors of the study with those published by the OECD confirms the relevance of the initial data, the results obtained, and the methodology used

.

After verifying the adequacy of the results obtained by the Authors, we can proceed to a more detailed analysis of them in order to identify trends and patterns.

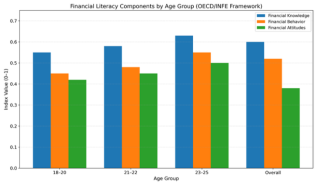

A comparison of three key components of financial literacy among young people of different ages in Ukraine showed that the index steadily increases with age.

Figure 3 illustrates that the 18–20 age group has the lowest level of knowledge, while the 23–25 age group has the highest level of knowledge. This suggests that theoretical financial knowledge is acquired through experience, education, or work experience.

The level of practical application of financial knowledge (budgeting, independence, and financial responsibility) remains the lowest among all three components. It is particularly low in the 19–22 age group, which may be related to the transition from student to professional life. The Financial Attitudes Index assesses attitudes related to financial risks (awareness of inflation, devaluation) and confidence in making financial decisions. Its highest values are again in the older 23–25 age group, reflecting greater awareness of financial reality. The lowest value is in the 19–22 age group.

Figure 3. The Authors Conducted a Comparison of Three Key Components of Financial Literacy Among Young People of Different Ages in Ukraine.

The data presented in the figure show that financial literacy can be improved through a consistent combination of theory and practice. Based on the data presented, we can conclude that the financial literacy of young people increases with age, but unevenly. Knowledge is formed faster than skills and attitudes, which is a natural process of acquiring any new skills. The most significant gap is observed between knowledge and behavior, which confirms the need for practical training. Financial attitudes develop slowly and are closely linked to the experience of making independent financial decisions.

3.2. Correlation Analysis of Socio-Economic Determinants of Financial Literacy

To investigate the relationships between the socio-economic characteristics of respondents and their level of financial literacy in greater detail, we employed correlation and regression analysis methods in our study.

Correlation analysis was performed using Pearson's coefficient to identify the direction and strength of the relationship between individual components of financial literacy. In particular, the analysis covered variables such as financial independence, budgeting ability, knowledge of basic economic concepts (including inflation, devaluation, and investment), and an integrated financial literacy index. The correlation matrix enabled us to identify the strongest links between theoretical knowledge and the behavioral characteristics of respondents. In particular, a moderate positive correlation was found between confidence in one's own knowledge and the actual level of literacy. The primary goal of the correlation analysis was to determine which variables have the most decisive influence on the overall level of financial literacy.

The correlation dependence was calculated for the following coefficients:

1) age ↔ integral indicator

2) self-assessment of knowledge ↔ behavioral skills

3) budgeting ↔ financial independence.

Calculations were performed for all pairs of variables that had a numerical or binary representation, followed by visualization in the form of a heat map.

The Pearson formula for our study was as follows:

(2)

Where:

xi, yi — values of variables X and Y for the i-th respondent

xˉ, yˉ — mean values of the corresponding variables

n — number of observations,

r{xy} — correlation coefficient between X and Y.

The expected results will be interpreted according to the following algorithm:

r{xy} = +1 — perfectly linear relationship (the greater X, the greater Y),

r{xy} = −1 — perfect inverse relationship (the greater X, the smaller Y),

r{xy} = 0 — lack of linear connection.

Our hypothesis was that the older the respondent, the higher their total score.

The correlation matrix, visualized as a heatmap, is shown in

Figure 4.

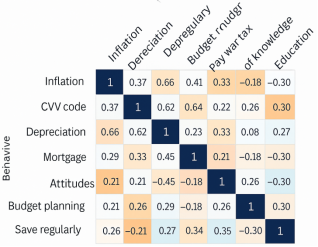

Figure 4. Correlation Matrix of Financial Variables (N=048) in the Form of a Heat Map Built by the Authors.

On the heat map, color intensity reflects the strength and direction of the relationship between variables. Yellow shades indicate a positive correlation, blue shades indicate a negative correlation, and tone saturation indicates the strength of the relationship. The values of the coefficients range from -1 to +1.

This matrix reflects the interrelationships between key indicators of financial literacy among young people, which are divided into three groups in accordance with the OECD structure:

Knowledge: knowledge about inflation, CVV codes, devaluation, mortgages, etc.

Behavior: budget planning, regular savings, payment of military tax.

Attitudes: self-assessment of knowledge, financial independence, and education.

The correlation matrix shows the strongest links:

1) The integrated assessment has a strong positive correlation with basic knowledge (r ≈ 0.86) and behavioral skills (r ≈ 0.75);

2) Basic knowledge is moderately correlated with knowledge of mortgages, inflation, CVV, and investments — r ≈ 0.40–0.55;

3) Behavioral skills correlate most strongly with self-assessment of knowledge (r ≈ 0.45), budget planning (r ≈ 0.42), and financial independence (r ≈ 0.35).

The authors drew the following main conclusions from the matrix.

First, a high correlation was found within knowledge blocks. For example, knowledge about inflation, devaluation, and CVV has correlations > 0.6. This may indicate consistent assimilation of basic terms: if a person knows one concept, there is a high probability that they also know related concepts.

Second, there is a weak link between knowledge and behavior. Correlations between knowledge (e.g., about mortgages) and practices (such as savings and tax obligations) are below 0.3. This means that knowledge does not always translate into financial behavior — a phenomenon known as the "behavioral gap."

Third, a moderate correlation has been established between financial independence and attitudes. The correlation between financial independence and higher education, or self-assessment of knowledge, is ~0.4–0.5. This may suggest the impact of educational status on the autonomy of young people in financial decision-making.

Finally, there is a low correlation between attitudes and behavior. For example, a feeling of lack of knowledge is not always accompanied by a change in behavior — the correlation between savings and self-assessment of knowledge is close to zero. This indicates the need for educational intervention that not only increases knowledge but also shapes beliefs and motivation.

3.3. Analysis Based on Multivariate Linear Regression

Multivariate linear regression was used to quantify the impact of individual socio-demographic factors on the level of financial literacy. The dependent variable was the constructed integral indicator of financial literacy, calculated based on nine criterion variables. The independent variables included: the respondent's approximate age (based on age category), level of education, degree of financial independence, budget planning horizon, and self-assessment of financial awareness.

The general model looks like:

R2 = 1.000 — The model perfectly explains the variation in the integral indicator (which is logical, since the variables in the model are the same nine indicators that make up the integral index). All coefficients are 0.1111, because the integral score is the average of the nine variables (i.e., each variable has the same weight: 19≈0.111191≈0.1111).

Linear regression model formula:

Y^=β0+β1X1+β2X2+β3X3+β4X4+β5X5(3)

Where:

y^ — predicted integral assessment of financial literacy

β0 — intercept, baseline literacy level when all factors are zero

X1 — respondent's age (conditional middle of age category)

X2 — level of education (0 = studying, 1 = bachelor's degree, 2 = master's degree)

X3 — financial independence (0 = dependent, 1 = partial, 2 = complete)

X4— budgeting horizon (0 = no plans, 1 = week, 2 = month, 3 = long term)

X5 — confidence in knowledge (0 = will seek help, 1 = partially confident, 2 = completely confident).

Under these conditions, the regression equation will be as follows:

Y^=0.492+(0.0006)X1+(0.0000)X2+(0.0278)X3−(0.0037)X4+ (0.0529)X5(4)

The interpretation of the coefficients is presented in

Table 4.

Table 4. Interpretation of Linear Regression Coefficients.

Element | Designation | Meaning | Explanation |

Intercept | β0 | 0.492 | Basic literacy level in the absence of all factors (hypothetically) |

Age | β1 | 0.0006 | Almost no effect (p = 0.96), effect is insignificant |

Education | β2 | ~0.0000 | Low effect (p ≈ 0.054), insignificant but borderline |

Independence | β3 | 0.0278 | Moderate positive effect, but statistically insignificant (p = 0.177) |

Budgeting | β4 | –0.0037 | Virtually zero and insignificant impact |

Confidence in knowledge | β5 | 0.0529 | The most significant predictor (p = 0.004). With each unit of confidence growth, the integral score increases by ≈5.3%. |

The model has limited explanatory power (R2 = 13.8%), but this is acceptable for social research. The strongest factor is psychological confidence, which confirms the importance not only of knowledge but also of subjective feelings of competence.

The model revealed a statistically significant impact of only one variable—confidence in one's own financial knowledge: each additional unit of confidence (on a scale from 0 to 2) is associated with an increase in the integral indicator by 0.053 (p < 0.01). Other variables (age, education, financial independence, and budget planning) did not show a statistically significant impact within the model. The only clearly substantial predictor of financial literacy is confidence in knowledge. Other variables (age, budgeting, independence) did not show a statistically significant effect in this model, although they make sense in theory.

4. Discussion

The findings of this study confirm a positive relationship between financial literacy and the level of financial inclusion among Ukrainian youth. The integrated score of 59.1% indicates a moderate level of financial capability, comparable to countries such as Brazil, Portugal, and Lithuania

. However, the observed gap between theoretical knowledge and practical behavior suggests that knowledge alone does not necessarily translate into sound financial habits.

These findings align with Sari & Mubarokah et al. (2025), who note that even well-informed youth often fail to adopt consistent saving and budgeting behaviors

| [8] | Mubarokah, S., Sari, P. P., & Kusumawardhani, R. (2024). The Influence of Digital Financial Literacy on Saving Behavior Among Gen Z in Indonesia. Indonesian Journal of Economics, Business, Accounting, and Management (IJEBAM), 2(5), 39-47. https://doi.org/10.63901/ijebam.v2i5.86 |

[8]

. Similarly, Linge et al. emphasize the role of financial attitudes – specifically confidence and awareness – as a decisive factor in shaping financial behaviors

| [18] | Linge, A. A., Kakde, B. B., & Jiwani, A. (2025). Factors Affecting Financial Literacy and Financial Behavior of Working Young Adults in India, Indian Journal of Finance. 2025, 19(11), 41-64.

https://doi.org/10.17010/ijf/2025/v19i11/174049 |

[18]

.

Our regression analysis identified self-confidence in financial knowledge as the only statistically significant predictor, confirming the conclusions of Rahmawati et al., who found that psychological factors often outweigh formal education in determining financial behavior

. This highlights the need for educational programs that foster not only knowledge but also subjective financial confidence.

Furthermore, Prihatiningsih & Pradana emphasize the need to equip youth with digital tools for self-managed financial behavior

| [7] | Prihatiningsih, P., & Pradana, M. R. A. Gen Z crypto investment: The role of FOMO, influencer, return, and financial literacy, Indonesian Journal of Banking and Financial Technology. 2025. https://doi.org/10.55927/fintech.v3i4.110 |

[7]

. In the Ukrainian context, particularly under the pressures of war and migration, fintech solutions can serve as a substitute for traditional banking access that has been disrupted

| [20] | Shahen, A. M., & Sharaf, M. F. The role of digital payment technologies in promoting financial inclusion: A systematic literature review, FinTech. 2025, 4(4), Article 59.

https://doi.org/10.3390/fintech4040059 |

[20]

.

A comparison with previous surveys (NBU, OECD, 2021) reveals a 2% increase in financial literacy over three years, indicating resilience and adaptability among youth despite external shocks

. This trend underscores the importance of digital platforms and informal learning in fostering financial empowerment.

5. Conclusions

The study's results indicate a positive correlation between the level of financial literacy among young people in Ukraine and their financial inclusion. An integrated index based on the OECD methodology showed an average level of financial literacy of 59.1%, meeting the basic international criteria. The highest scores were found in the area of theoretical financial knowledge. In contrast, practical behavior and financial attitudes were less developed, indicating the existence of a so-called "behavioral gap" — a gap between knowledge and its application. This thesis is confirmed by a correlation analysis, which revealed a weak link between knowledge and behavior.

A comparative analysis with previous studies on financial literacy levels in Ukraine (2020–2021) reveals a gradual positive trend among young people, despite the war, economic turbulence, and changes in infrastructure conditions. These results demonstrate the adaptability of the younger generation to crisis-induced changes, particularly through the use of digital financial tools.

Regression analysis confirmed that the most significant predictor of financial inclusion is psychological confidence in one's own financial knowledge, while other socio-demographic factors (age, level of education, degree of independence) proved to be statistically insignificant within this model. This indicates the need not only for information campaigns, but also for educational programs aimed at strengthening the subjective sense of financial capability.

The findings have significant practical value for the development of national financial strategy, digital inclusion, educational initiatives, and regional financial stability programs. They also confirm that financial literacy is not only a tool for accessing services, but also a key factor in socio-economic self-sufficiency and human capital development. It is the financial awareness of young people that can lay a solid foundation for the future development of the country's adult population. Their effective financial behavior will ensure the stability of both the financial system and the country's economic potential, resulting from the population's adequate and responsible financial behavior. Further research in the field of financial literacy and financial inclusion has practical applications in the context of the country's population's socio-economic stability.

Abbreviations

OECD | Organisation for Economic Co-operation and Development |

INFE | International Network on Financial Education |

G20 | Group of Twenty |

SDGs | Sustainable Development Goals |

NBU | National Bank of Ukraine |

USAID | United States Agency for International Development |

OLS | Ordinary Least Squares |

CVV | Card Verification Value |

Author Contributions

Viktoriia Rudevska: Conceptualization, Formal Analysis, Methodology, Project administration, Validation, Writing– review & editing

Kateryna Ukhanova: Data curation, Visualization, Writing – original draft

Data Availability Statement

The data is available from the corresponding author upon reasonable request.

Conflicts of Interest

The authors declare no conflicts of interest.

References

| [1] |

Bilous I. I. Financial literacy as the basis for ensuring the financial security of households, Collection of scientific papers LOGOS. 2020, 59-62.

https://doi.org/10.36074/21.02.2020.v1.17

|

| [2] |

OECD. Financial Inclusion and Consumer Empowerment in the Digital Age. Organization for Economic Co-operation and Development. 2020. Available from:

https://www.oecd.org/finance/financial-inclusion-consumer-empowerment.html

(accessed 6 November 2025).

|

| [3] |

World Bank. 2025, January 27. Financial inclusion overview. The World Bank.

|

| [4] |

G20. High-Level Principles for Digital Financial Inclusion. Global Partnership for Financial Inclusion. 2016. Available from:

https://www.gpfi.org/publications/g20-high-level-principles-digital-financial-inclusion

(accessed 6 November 2025).

|

| [5] |

National Bank of Ukraine. (2023). National Strategy for Financial Literacy Development until 2030. Available from:

https://bank.gov.ua/ua/about/strategy-fin-literacy

(accessed 8 November 2025).

|

| [6] |

Mandal, B. K., Kumari, S., & Das, P. Impact of government-led saving initiative on women empowerment and financial inclusion in rural population: evidence from Amar Bari Amar Khamar (ABK) project in Bangladesh, Lex localis-journal of local self-governmen, Vol. 23, NS3 (2025)

https://lex-localis.org/index.php/LexLocalis/article/view/800643/1415

|

| [7] |

Prihatiningsih, P., & Pradana, M. R. A. Gen Z crypto investment: The role of FOMO, influencer, return, and financial literacy, Indonesian Journal of Banking and Financial Technology. 2025.

https://doi.org/10.55927/fintech.v3i4.110

|

| [8] |

Mubarokah, S., Sari, P. P., & Kusumawardhani, R. (2024). The Influence of Digital Financial Literacy on Saving Behavior Among Gen Z in Indonesia. Indonesian Journal of Economics, Business, Accounting, and Management (IJEBAM), 2(5), 39-47.

https://doi.org/10.63901/ijebam.v2i5.86

|

| [9] |

World Bank. Financial Inclusion. Financial inclusion is a key enabler to reducing poverty and boosting prosperity.

|

| [10] |

United Nations. Take Action for the Sustainable Development Goals. Available from:

https://www.un.org/sustainabledevelopment/sustainable-development-goals/

(accessed 8 November 2025).

|

| [11] |

Setiawati, N. T. and Primadineska, R. W. Financial Behavior of Generation Z in Indonesia: Impact of Literacy, Technology and Lifestyle, Telaah Bisnis. 2025, 2 6, 55-68.

https://doi.org/10.35917/tb.v26i1.596

|

| [12] |

Tkachuk, N., Novosad, O. Formation of the key competence “entrepreneurship and financial literacy” in the educational process in geography, Scientific Notes of Vinnytsia State Pedagogical University named after Mykhailo Kotsyubinsky. Series: Theory and Methods of Teaching Natural Sciences. 2024, 7, 22-31.

https://doi.org/10.31652/2786-5754-2024-7-22-31

|

| [13] |

Yevtushenko, N., Stetsenko, D. Financial Inclusion in Ukraine: Current Status and Prospects for Development, Grail of Science. 18 Jun. 2024, 40, 136-140.

https://doi.org/10.36074/grail-of-science.07.06.2024.015

|

| [14] |

Krupka, M., Zamaslo, O., Petyk, M., Diuh, I. Financial Sustainability of Local Budgets in Ukraine in the Context of Financial Inclusion and Post-War Economic Recovery, World of Finance. 2025, 3(84), 08-23.

https://doi.org/10.35774/sf2025.03.008

|

| [15] |

Vidiati, C., Nursindi, M. The Role of Digital Islamic Economics in Increasing Financial Inclusion in the Fintech Era, Advances in Social Humanities Research. 2024, 2(12), 2279-2289.

|

| [16] |

OECD/INFE 2023 International Survey of Adult Financial Literacy. Available from:

https://www.oecd.org/en/publications/oecd-infe-2023-international-survey-of-adult-financial-literacy_56003a32-en.html

(accessed 12 November 2025).

|

| [17] |

OECD/INFE 2018 Toolkit for Measuring Financial Literacy and Financial Inclusion. Available from:

https://www.oecd.org/financial/education/2018-INFE-FinLit-Measurement-Toolkit.pdf

(accessed 12 November 2025).

|

| [18] |

Linge, A. A., Kakde, B. B., & Jiwani, A. (2025). Factors Affecting Financial Literacy and Financial Behavior of Working Young Adults in India, Indian Journal of Finance. 2025, 19(11), 41-64.

https://doi.org/10.17010/ijf/2025/v19i11/174049

|

| [19] |

Rahmawati, D., Sutanto, M. R., & Hartono, Y. Self-efficacy and Financial Decision Making in Young Adults, Journal of Financial Education and Development. 2024, 10(1), 67-83.

https://doi.org/10.20885/jielariba.vol11.iss2.art16

|

| [20] |

Shahen, A. M., & Sharaf, M. F. The role of digital payment technologies in promoting financial inclusion: A systematic literature review, FinTech. 2025, 4(4), Article 59.

https://doi.org/10.3390/fintech4040059

|

Cite This Article

-

APA Style

Rudevska, V., Ukhanova, K. (2026). Financial Literacy as a Driver of Financial Inclusion and Economic Empowerment: Empirical Evidence from Ukrainian Youth. International Journal of Economics, Finance and Management Sciences, 14(1), 58-68. https://doi.org/10.11648/j.ijefm.20261401.15

Copy

|

Copy

|

Download

Download

ACS Style

Rudevska, V.; Ukhanova, K. Financial Literacy as a Driver of Financial Inclusion and Economic Empowerment: Empirical Evidence from Ukrainian Youth. Int. J. Econ. Finance Manag. Sci. 2026, 14(1), 58-68. doi: 10.11648/j.ijefm.20261401.15

Copy

|

Download

AMA Style

Rudevska V, Ukhanova K. Financial Literacy as a Driver of Financial Inclusion and Economic Empowerment: Empirical Evidence from Ukrainian Youth. Int J Econ Finance Manag Sci. 2026;14(1):58-68. doi: 10.11648/j.ijefm.20261401.15

Copy

|

Download

-

@article{10.11648/j.ijefm.20261401.15,

author = {Viktoriia Rudevska and Kateryna Ukhanova},

title = {Financial Literacy as a Driver of Financial Inclusion and Economic Empowerment: Empirical Evidence from Ukrainian Youth},

journal = {International Journal of Economics, Finance and Management Sciences},

volume = {14},

number = {1},

pages = {58-68},

doi = {10.11648/j.ijefm.20261401.15},

url = {https://doi.org/10.11648/j.ijefm.20261401.15},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijefm.20261401.15},

abstract = {This study investigates the role of financial literacy as a key driver of financial inclusion and behavioral empowerment among Ukrainian youth in the context of digital transformation and post-crisis economic recovery. Based on a large-scale survey of 948 respondents aged 18–25, the research employs an integrated methodological framework that combines index modeling, correlation analysis, and multivariate linear regression. Financial literacy is operationalized through a composite index constructed in accordance with the OECD/INFE methodology, incorporating financial knowledge, financial behavior, and financial attitudes. The results indicate a moderate overall level of financial literacy among Ukrainian youth, with an average index value of 0.591 on a normalized scale of 0–1. While theoretical financial knowledge demonstrates relatively stronger performance, practical financial behavior and attitudinal confidence remain comparatively weaker, revealing a persistent behavioral gap between awareness and action. Correlation analysis confirms strong internal consistency within the knowledge and behavior components, but only limited spillover from knowledge to real financial practices. Regression estimates reveal that self-confidence in personal financial knowledge is the only statistically significant predictor of financial inclusion (β = 0.0529, p < 0.01), whereas age, formal education, budgeting horizon, and financial independence exhibit no robust explanatory power. This finding highlights the decisive role of psychological factors in shaping financial behavior beyond formal human capital characteristics. The findings confirm that financial literacy influences financial inclusion not primarily through formal knowledge or education, but through psychological confidence and subjective financial capability. Access to financial services alone is insufficient without behavioral readiness and autonomy in decision-making. The study provides empirical evidence that confidence-oriented financial education, combined with digital financial infrastructure, is crucial for promoting sustainable financial inclusion among young people. These findings carry important implications for public policy in post-war and transition economies, emphasizing the need for integrated national strategies that link education, digitalization, and behavioral empowerment.},

year = {2026}

}

Copy

|

Download

-

TY - JOUR

T1 - Financial Literacy as a Driver of Financial Inclusion and Economic Empowerment: Empirical Evidence from Ukrainian Youth

AU - Viktoriia Rudevska

AU - Kateryna Ukhanova

Y1 - 2026/02/02

PY - 2026

N1 - https://doi.org/10.11648/j.ijefm.20261401.15

DO - 10.11648/j.ijefm.20261401.15

T2 - International Journal of Economics, Finance and Management Sciences

JF - International Journal of Economics, Finance and Management Sciences

JO - International Journal of Economics, Finance and Management Sciences

SP - 58

EP - 68

PB - Science Publishing Group

SN - 2326-9561

UR - https://doi.org/10.11648/j.ijefm.20261401.15

AB - This study investigates the role of financial literacy as a key driver of financial inclusion and behavioral empowerment among Ukrainian youth in the context of digital transformation and post-crisis economic recovery. Based on a large-scale survey of 948 respondents aged 18–25, the research employs an integrated methodological framework that combines index modeling, correlation analysis, and multivariate linear regression. Financial literacy is operationalized through a composite index constructed in accordance with the OECD/INFE methodology, incorporating financial knowledge, financial behavior, and financial attitudes. The results indicate a moderate overall level of financial literacy among Ukrainian youth, with an average index value of 0.591 on a normalized scale of 0–1. While theoretical financial knowledge demonstrates relatively stronger performance, practical financial behavior and attitudinal confidence remain comparatively weaker, revealing a persistent behavioral gap between awareness and action. Correlation analysis confirms strong internal consistency within the knowledge and behavior components, but only limited spillover from knowledge to real financial practices. Regression estimates reveal that self-confidence in personal financial knowledge is the only statistically significant predictor of financial inclusion (β = 0.0529, p < 0.01), whereas age, formal education, budgeting horizon, and financial independence exhibit no robust explanatory power. This finding highlights the decisive role of psychological factors in shaping financial behavior beyond formal human capital characteristics. The findings confirm that financial literacy influences financial inclusion not primarily through formal knowledge or education, but through psychological confidence and subjective financial capability. Access to financial services alone is insufficient without behavioral readiness and autonomy in decision-making. The study provides empirical evidence that confidence-oriented financial education, combined with digital financial infrastructure, is crucial for promoting sustainable financial inclusion among young people. These findings carry important implications for public policy in post-war and transition economies, emphasizing the need for integrated national strategies that link education, digitalization, and behavioral empowerment.

VL - 14

IS - 1

ER -

Copy

|

Download