1. Background

Despite its satirical title, this article does not claim that Sierra Leone has irreversibly failed in its currency redenomination. Instead, it offers a participatory review, rooted in legal analysis, policy evaluation, and public opinion, to critically assess whether the objectives of the currency redenomination have been genuinely achieved, fallen short, or misunderstood as a “technocratic economic gamble”(author’s emphasis).

By currency redenomination, scholars submit that it is a significant policy tool often employed by governments in both developing and transition economies as part of broader economic or political reform agendas. While perspectives may differ, a growing body of research affirms that redenomination is frequently introduced to restore macroeconomic credibility, simplify transactions, or signal a new phase of governance or fiscal discipline.

| [1] | Dogarawa AB, The Economics of Currency Redenomination: An Appraisal of CBN Redenomination Proposal (Ahmadu Bello University, Zaria-Nigeria 2007)

https://doi.org/10.2139/ssrn.1622144 |

[1]

It is further posited as the process through which a country recalibrates its currency, most often by removing zeros from the face value, in pursuit of targeted economic and fiscal objectives.

| [1] | Dogarawa AB, The Economics of Currency Redenomination: An Appraisal of CBN Redenomination Proposal (Ahmadu Bello University, Zaria-Nigeria 2007)

https://doi.org/10.2139/ssrn.1622144 |

[1]

.

In supporting their respective arguments, some scholars observe that currency redenomination is more than a technical adjustment; it is often employed by governments as a strategic response to economic instability, loss of monetary credibility, or hyperinflation.

| [1] | Dogarawa AB, The Economics of Currency Redenomination: An Appraisal of CBN Redenomination Proposal (Ahmadu Bello University, Zaria-Nigeria 2007)

https://doi.org/10.2139/ssrn.1622144 |

[1]

In some cases, it forms part of a broader economic or political reform agenda. For example, in Afghanistan, following years of conflict and currency depreciation, a new afghani was introduced in October 2002 with three zeros removed, as part of a wider reconstruction effort.

| [2] | Mosley L, ‘Dropping Zeros, Gaining Credibility? Currency Redenomination in Developing Nations’ (Paper presented at the 2005 Annual Meeting of the American Political Science Association, 2005). |

[2]

In Turkey, redenomination was used to restore the credibility of the national currency, which had suffered from prolonged inflation. In 2005, the Turkish government eliminated six zeros from the lira, rebranding it as the “New Turkish Lira” to signal a fresh economic start.

| [3] | Central Bank of the Republic of Turkey. (2006). Annual report 2006. Central Bank of the Republic of Turkey. |

[3]

Similarly, Zimbabwe and Ghana undertook redenomination to reassert monetary sovereignty and regain public confidence. Zimbabwe removed three zeros from its dollar, while Ghana dropped four zeros from the old cedi in 2007, replacing it with the Ghanaian New Cedi.

| [4] | Riki Matsumoto, ‘Examining the 2007 Redenomination of the Ghanaian Cedi on the Disinflation Process Using the Chow Structural Break Test and VAR’ (International Affairs & Economics, ESIA ‘18). |

[4]

.

Redenomination has also been used in response to hyperinflationary pressures, where the national currency becomes practically unusable. In Brazil, Argentina, and Peru, governments responded by introducing new currency units that removed excessive zeros to simplify transactions and reduce the psychological impact of inflation.

| [4] | Riki Matsumoto, ‘Examining the 2007 Redenomination of the Ghanaian Cedi on the Disinflation Process Using the Chow Structural Break Test and VAR’ (International Affairs & Economics, ESIA ‘18). |

[4]

.

In Venezuela, the years leading up to 2018 were marked by a severe economic crisis characterized by hyperinflation, a sharp decline in oil revenues, which are vital to the country’s income, shortages of essential goods, and worsening social conditions. To tackle these challenges, the government introduced a currency redenomination plan in 2018.

| [5] | Orozco, J., & Zerpa, F. (2018). Venezuela Delays New Currency Rollout, Slashes More Zeroes. |

[5]

This involved replacing the old currency, the Strong Bolivar (Bs.F), with the new Sovereign Bolivar (Bs.S) at a rate of 100,000 Bs.F to 1 Bs.S, effectively removing five zeros from the currency.

| [6] | Laya, P., & Vasquez, A. (2021). Venezuela to cut six zeroes off Bolivar to simplify transactions. |

[6]

.

While writers continue to posit their perceived reasons for redenomination, the above examples illustrate that redenomination, while involving a change in numerical value, is fundamentally a symbolic and practical tool for signaling reform, restoring confidence, and reaffirming a government's control over its monetary system.

| [6] | Laya, P., & Vasquez, A. (2021). Venezuela to cut six zeroes off Bolivar to simplify transactions. |

[6]

However, Nigeria’s attempt at currency redenomination offers a telling example of how economic policy can be both ambitious and contested. In August 2007, the Central Bank of Nigeria (CBN), under the leadership of Professor Charles Soludo, proposed a sweeping reform to restructure the naira by dropping two zeros—effectively moving the decimal point two places to the left. Under this plan, ₦100 would become ₦1, and ₦1 would equal 1 kobo, with a redesigned currency structure placing ₦20 as the highest denomination and 1 kobo as the lowest.

| [1] | Dogarawa AB, The Economics of Currency Redenomination: An Appraisal of CBN Redenomination Proposal (Ahmadu Bello University, Zaria-Nigeria 2007)

https://doi.org/10.2139/ssrn.1622144 |

[1]

This redenomination formed part of a broader 13-point reform agenda aimed at enhancing macroeconomic stability, revitalizing microfinance, reducing inflation, and promoting a more efficient payment system. The policy also sought to reintroduce coin usage and reduce the psychological burden of inflationary pricing. However, the proposal met with mixed reactions. While some praised it as a bold move that could strengthen the naira, curb capital flight, and limit the illicit accumulation of wealth, others criticized it for lacking adequate consultation and questioned its feasibility within Nigeria’s socio-political context. Ultimately, due to political, economic, and legal pressures, the reform was suspended before implementation.

| [1] | Dogarawa AB, The Economics of Currency Redenomination: An Appraisal of CBN Redenomination Proposal (Ahmadu Bello University, Zaria-Nigeria 2007)

https://doi.org/10.2139/ssrn.1622144 |

[1]

Nevertheless, the debate surrounding the proposal highlighted the symbolic power of currency in economic identity and trust—and Nigeria’s experience remains a crucial case study in how redenomination plans can falter not for lack of technical merit, but due to politico-economic resistance and institutional inertia.

| [1] | Dogarawa AB, The Economics of Currency Redenomination: An Appraisal of CBN Redenomination Proposal (Ahmadu Bello University, Zaria-Nigeria 2007)

https://doi.org/10.2139/ssrn.1622144 |

[1]

.

Down here in Sierra Leone, following the 2018 Presidential election, Professor Kelfala Morana Kallon was appointed Governor of the Bank of Sierra Leone, subject to parliamentary approval, effective August 15, 2018, pursuant to sections 15(1) and (2) of the Bank of Sierra Leone Act, 2011 now the Bank of Sierra Leone Act, 2019. One of his earliest policy initiatives was the implementation of monetary measures aimed at controlling inflation, curbing currency depreciation, and stabilizing the exchange rate. In line with several legislative measures, Sierra Leone undertook a bold monetary reform to drop three zeros from its currency; a move widely branded as a step toward achieving monetary stability. According to World Bank, after redenomination, Sierra Leone experienced a sharp rise in inflation, driven primarily by a combination of external shocks and expansionary fiscal and monetary policies.

| [7] | World Bank, Sierra Leone Economic Update: Enhancing Value Chains to Boost Food Security (October 2023) |

[7]

.

Pursuant to Public Notice No. 40, Vol. CXLXIII dated 16

th day of June 2022, the Bank of Sierra Leone announced that, pursuant to the Redenomination of the Leone (Characteristics) Regulations 2021, the redenominated currency became legal tender on the 1

st July 2022.

| [8] | Public Notice No 40, Vol CXLXIII (Sierra Leone, 16 June 2022). |

[8]

As one of the poorest countries in the world, the Bank of Sierra Leone under the leadership of the Governor argued that the old currency regime (the defunct Leone) imposed significant burdens on the economy. These included high transaction costs, general inconvenience, and increased risks associated with carrying large volumes of cash for everyday transactions.

| [9] | Bank of Sierra Leone, 'Frequently Asked Questions on the Redenomination of the Leone' (March 2022). |

[9]

Additional challenges cited were difficulties in maintaining accurate bookkeeping and statistical records, problems with accounting and data processing systems, and a considerable strain on the national payment infrastructure.

| [9] | Bank of Sierra Leone, 'Frequently Asked Questions on the Redenomination of the Leone' (March 2022). |

[9]

.

2. Theoretical Foundations of Regulatory Policy

The development of regulations, whether monetary or not, has long been a subject of academic inquiry, particularly in assessing their impact on targeted sectors. In this context, regulation refers to the use of legal instruments to implement socio-economic policy objectives.

| [10] | J. A. den Hertog, 2010. "Review of economic theories of regulation," Working Papers 10-18, Utrecht School of Economics. (8). |

[10]

These legal tools serve as mechanisms through which governments seek to guide economic and social activities in line with broader developmental goals.

Two main schools of thought underpin regulatory policy: positive theories of regulation and normative theories of regulation.

| [10] | J. A. den Hertog, 2010. "Review of economic theories of regulation," Working Papers 10-18, Utrecht School of Economics. (8). |

[10]

These frameworks guide the design of regulations to serve either public or private interests. By applying these theories, policymakers and stakeholders in affected sectors can better assess the relevance and effectiveness of regulatory measures.

| [10] | J. A. den Hertog, 2010. "Review of economic theories of regulation," Working Papers 10-18, Utrecht School of Economics. (8). |

[10]

The positive theory of regulation, also known as the public interest theory, focuses on the economic explanations for regulation and its consequences.

| [10] | J. A. den Hertog, 2010. "Review of economic theories of regulation," Working Papers 10-18, Utrecht School of Economics. (8). |

[10]

The theory seeks to explain why regulation occurs, encompassing theories of market power, interest group theories that describe stakeholders’ influence on regulation, and theories of government opportunism which argue that restricting government discretion may be necessary to ensure efficient service delivery in regulated sectors.

| [10] | J. A. den Hertog, 2010. "Review of economic theories of regulation," Working Papers 10-18, Utrecht School of Economics. (8). |

[10]

Shleifer asserts that this theory has been employed both as a normative prescription of what governments should do and descriptively to explain what governments actually do, particularly in democratic countries.

| [11] | Mulligan, Casey, and Andrei Shleifer. 2005. “The Extent of the Market and the Supply of Regulation.” Quarterly Journal of Economics 120(4): 1445-1473. |

[11]

Knieps however, views the positive theory of regulation as encompassing the emergence, transformation, abolition, and institutional implementation of sector-specific regulation.

The central question in this view is how network industries are actually regulated in practice.

.

Generally, the positive theory concludes that regulation occurs because governments aim to overcome information asymmetries with operators and align the operators’ interests with those of the government. Additionally, consumers seek protection from market power in cases where competition is absent or ineffective, operators desire protection from rivals, and operators may also seek protection from government opportunism.

| [13] | H Th A Bressers and P-J Klok, ‘Fundamentals for a Theory of Policy Instruments’ (1988) 15(3–4) International Journal of Social Economics 22–41. |

[13]

.

Despite these insights, the Chicago School of Law and Economics has criticized positive theory on several grounds. Their critique unfolds in three intellectual steps. First, they argue that markets and private orderings can address most market failures without the need for government intervention or regulation. Second, where markets do not function perfectly, private litigation is seen as an effective mechanism to resolve conflicts among market participants. Third, even if markets and courts are imperfect, government regulators are viewed as generally incompetent, corrupt, or subject to capture, meaning that regulation could potentially worsen the situation.

| [11] | Mulligan, Casey, and Andrei Shleifer. 2005. “The Extent of the Market and the Supply of Regulation.” Quarterly Journal of Economics 120(4): 1445-1473. |

[11]

.

The normative theory of regulation, in contrast, investigates which types of regulation are most efficient, operating under the implicit assumption that efficient regulation is desirable. It conducts a cost-benefit analysis of various regulatory instruments and frameworks.

| [11] | Mulligan, Casey, and Andrei Shleifer. 2005. “The Extent of the Market and the Supply of Regulation.” Quarterly Journal of Economics 120(4): 1445-1473. |

[11]

Normative theories generally conclude that regulators should encourage competition where feasible, minimize the costs of information asymmetries by acquiring necessary information and providing incentives to operators to improve performance, establish price structures that enhance economic efficiency, and ensure that regulatory processes are conducted under the rule of law with independence, transparency, predictability, legitimacy, and credibility.

2.1. Regulatory Governance for Broader Economic Reforms

Regulatory Policy has been fundamental to governing complex, open and diverse societies and economies by allowing policy-makers to balance competing interests in the development of democracies and the market economies.

| [14] | Organisation for Economic Co-operation and Development, 'Regulatory Impact Analysis in OECD Countries: Challenges for Developing Countries' (South Asian-Third High Level Investment Roundtable, Dhaka, Bangladesh, June 2005). |

[14]

In this regard, in the early years of the 20th Century, the growth of regulatory systems was an unplanned expansion into more areas in response to problems and the complexity of economic and social activities.

| [14] | Organisation for Economic Co-operation and Development, 'Regulatory Impact Analysis in OECD Countries: Challenges for Developing Countries' (South Asian-Third High Level Investment Roundtable, Dhaka, Bangladesh, June 2005). |

[14]

However, the emergence of regulatory reform and deregulation in the 1970s according to the Organisation for Economic Co-operation and Development (hereinafter referred to as OECD), constituted the first explicit and sustained attempt to understand the nature of regulation and its limits as a policy instrument.

| [14] | Organisation for Economic Co-operation and Development, 'Regulatory Impact Analysis in OECD Countries: Challenges for Developing Countries' (South Asian-Third High Level Investment Roundtable, Dhaka, Bangladesh, June 2005). |

[14]

Equally, as more was learnt about the nature of the regulatory tools in the 1980s and the 1990s, deregulation gave way to regulatory reform, then to regulatory management and, more recently, to a forward-looking agenda to improve regulatory policies and governance

| [14] | Organisation for Economic Co-operation and Development, 'Regulatory Impact Analysis in OECD Countries: Challenges for Developing Countries' (South Asian-Third High Level Investment Roundtable, Dhaka, Bangladesh, June 2005). |

[14]

.

According to the International Monetary Funds, (hereinafter referred to as IMF), good regulatory governance in the financial system is a critical component of financial stability.

It follows the view that a financial system is only as strong as its governance practices, the financial soundness of its institutions, and the efficiency of its market infrastructure. Thus, ensuring and applying sound governance practices is a shared responsibility between market participants and regulatory agencies.

For the purposes of this article, regulatory governance applies to the Bank of Sierra Leone that possesses legal powers to regulate, supervise and/or intervene in the financial sector.

The OECD argues that appropriately designed and well-implemented regulations of any kind serve as powerful tools for enhancing economic performance and societal well-being.

The OECD further posits that, a strong and sound regulatory framework can mitigate threats to public health, safety, and the environment, while addressing market imperfections.

These regulatory benefits extend throughout the economy, fostering sustained economic growth.

Within the purviews of currency redenomination, regulatory governance remains more than a mere technical exercise of changing a nation’s monetary unit; it steps towards the bounds of a strategic policy intervention with significant economic, social, and legal implications.

The success or failure of such a reform hinges on the strength, clarity, and enforcement of its underlying legal and regulatory frameworks. It is therefore posited that regulatory governance in respect of currency redenomination refers to the system of laws, policies, institutions, and procedures that oversee, guide, and ensure the effective design, implementation, and monitoring of the redenomination process. It involves setting clear legal frameworks and regulatory standards to manage the transition to a new currency scale, ensuring transparency, accountability, and coordination among monetary authorities, government agencies, financial institutions, and the public.

Promoting good regulatory governance has become a key priority for the IMF and other international financial institutions (IFIs). Focusing primarily on the economic aspects of governance, the IMF advances good regulatory governance through several instruments. These include: (i) providing advice and technical assistance to strengthen policymaking institutions such as central banks and regulatory bodies; (ii) enhancing integrity and transparency in financial transactions by conducting safeguards assessments and promoting good transparency practices in fiscal, monetary, and financial policies; and (iii) evaluating anti-money laundering supervisory regimes and monitoring measures implemented to combat the financing of terrorist activities by financial intermediaries.

Thus the effectiveness of a regulatory framework depends on both

what is regulated and

how the regulation is designed and implemented. Policymakers and regulators must carefully consider the

substance of regulation, the “rules of the game”, to ensure they achieve the desired outcomes. Equally important is attention to

how regulations are developed, implemented, and reviewed, as this process determines whether the regulations function effectively to promote the public interest.

.

Finally, Good regulatory governance in this context would aim to minimize economic disruptions, maintain public trust, and support macroeconomic stability by providing clear rules on the issuance of new currency notes and coins, managing the withdrawal of old currency, controlling inflationary risks, and facilitating public awareness and compliance.

2.2. Understanding the Concept, History and Lessons from Currency Redenomination

Currency redenomination, as indicated earlier, is a critical monetary reform tool often employed to simplify transactions, rebuild public confidence, and reinforce broader macroeconomic stabilization strategies. It is a process whereby a country’s currency is recalibrated (i) due to significant inflation and currency devaluation, (ii) when a currency union is formed, (iii) when a currency union breaks up.

| [17] | Roberto A De Santis, ‘A Measure of Redenomination Risk’ (Working Paper Series 1785, European Central Bank, April 2015). |

[17]

Typically, it involves adjusting the nominal value of a currency by removing one or more zeros, while maintaining its real purchasing power.

| [17] | Roberto A De Santis, ‘A Measure of Redenomination Risk’ (Working Paper Series 1785, European Central Bank, April 2015). |

[17]

For such reform to yield meaningful results, however, it must be underpinned by a robust legal framework, strategic economic policies, and effective public communication.

| [17] | Roberto A De Santis, ‘A Measure of Redenomination Risk’ (Working Paper Series 1785, European Central Bank, April 2015). |

[17]

.

As Kargbo and Gbolonyo note, the practice of redenomination has a long and varied history, dating back to 1892 when Austria-Hungary adopted a monetary union and shifted from the silver to the gold standard.

| [18] | Kargbo, B. I. B., & Gbolonyo, E. Y. (2023). Dropping the Ze roes: Between Hope and Reality for Sierra Leone: A Critical Review of the Literature. Modern Economy, 14, 163-177.

https://doi.org/10.4236/me.2023.142011 |

[18]

Since then, numerous countries have undertaken redenomination for economic, political, or symbolic purposes.

| [18] | Kargbo, B. I. B., & Gbolonyo, E. Y. (2023). Dropping the Ze roes: Between Hope and Reality for Sierra Leone: A Critical Review of the Literature. Modern Economy, 14, 163-177.

https://doi.org/10.4236/me.2023.142011 |

[18]

Although often presented as a technical intervention, the decision to redenominate is inherently political—reflecting a government's assertion of monetary sovereignty, particularly in times of economic distress or civil instability.

| [19] | Woodruff, D. (1999). Money Unmade. Ithaca: Cornell University Press. |

[19]

.

The experiences of countries such as Afghanistan, Turkey, Angola, Mozambique, Brazil, and Argentina, underscore that redenomination is most effective when it forms part of a comprehensive suite of structural reforms.

| [19] | Woodruff, D. (1999). Money Unmade. Ithaca: Cornell University Press. |

[19]

When pursued in isolation, redenomination can become merely cosmetic, offering little more than psychological reprieve without substantive economic transformation. In such cases, countries risk falling into a pattern of "redenomination-mania"—the repeated urge to redenominate in response to unresolved macroeconomic dysfunctions.

| [20] | Sesay, D. K., Bah, C. J., Mansaray, I., & Kanu, A. S. (2022). Assessing the Impact of Cur rency Redenomination: An Appraisal of the Bank of Sierra Leone’s Redenomination Proposal. International Journal of Multidisciplinary Research and Growth Evaluation 1, 328-331. |

[20]

.

As Kaindoh argues, the empirical lessons from successful redenomination efforts reveal a consistent set of prerequisites: macroeconomic stability, institutional and legal readiness, inclusive stakeholder engagement, and properly sequenced implementation.

| [21] | Kaindoh J, 'Insight into Sierra Leone’s Currency Redenomination' (Sierraloaded, 2022). |

[21]

Despite access to this global pool of knowledge, Sierra Leone’s redenomination effort appeared to bypass several of these critical elements. Below are some success lessons:

Ghana (2007)

Ghana undertook a widely cited and generally successful redenomination in 2007. Faced with an over-inflated currency, it removed four zeros, converting 10,000 old Cedis to 1 new Ghana Cedi (GHS). The process included strong public education campaigns, a well-coordinated transition led by the Bank of Ghana, and legal adjustments to accommodate the change. The impact was largely positive: transactions were simplified, investor confidence improved, and inflation was kept in check due to effective communication and sound macroeconomic management.

| [22] | Dzokoto, V. A. A., Mensah, E. C., Twum-Asante, M. and Opare-Henaku, A. (2010a) ‘Deceiving our minds: a qualitative exploration of the money illusion in post-redenomination Ghana’, Journal of Consumer Policy, Vol. 33, No. 4, pp. 339–353. |

[22]

.

Turkey (2005)

Turkey removed six zeros from its Lira, introducing the New Turkish Lira (YTL) at a conversion rate of 1 YTL = 1,000,000 old Lira. Like Ghana, the redenomination was part of a broader economic stabilization package. Turkey passed enabling legislation early, rolled out extensive public education, and updated financial systems. This initiative helped restore public confidence and facilitated economic recovery and international investment appeal.

| [23] | Central Bank of the Republic of Turkey, Redenomination of Turkish Lira by Dropping Six Zeros (2004a). |

[23]

.

Zimbabwe (2006–2009)

In stark contrast, Zimbabwe’s multiple redenominations failed to yield positive results. Repeated removal of zeros, without addressing structural causes of hyperinflation, eroded public trust and worsened economic instability.

| [2] | Mosley L, ‘Dropping Zeros, Gaining Credibility? Currency Redenomination in Developing Nations’ (Paper presented at the 2005 Annual Meeting of the American Political Science Association, 2005). |

[2]

By 2009, the Zimbabwean dollar was abandoned in favor of a multi-currency system.

| [24] | Nawa Mutumwena, ‘Zambia redenominates the kwacha: Zambia has finally agreed to redenominate its currency, which, following periods of inflation, has become unwieldy’ African Business (1 March 2012). |

[24]

.

Brazil (1994)

Brazil's “Plano Real” introduced a virtual unit of account (URV) before launching the Real (BRL) in 1994. This transitional strategy stabilized expectations and smoothed the redenomination. The plan also involved strict fiscal and monetary reforms and extensive public education, resulting in significant reduction in hyperinflation and restored public trust.

| [25] | Leslie Elliott Armijo, ‘Inflation and Insouciance: The Peculiar Brazilian Game’ (1996) 31(3) Latin American Research Review 7–46. |

[25]

.

Venezuela (2018)

Venezuela redenominated its currency by removing five zeros, introducing the Sovereign Bolivar. However, the move was largely symbolic, as hyperinflation continued due to lack of credible monetary and fiscal reforms.

| [26] | Patricia Laya and Alex Vasquez, ‘Maduro’s reluctant reforms may halt Venezuelan economic freefall’ (Bloomberg, 22 June 2021). |

[26]

The abrupt nature of the policy caused confusion, and inflationary pressures eroded any short-term gains.

| [27] | Patricia Laya, “Venezuela to Cut Six Zeroes Off Bolivar to Simplify Transactions” (Bloomberg, 1 July 2021). |

[27]

.

Argentina (Multiple Instances)

Argentina’s experience shows the complexities of currency reform amid political and economic instability. Despite some short-term gains through pegging to the US dollar, inflexible policies and rising debt led to collapse of the Convertibility Plan. Public confidence declined as fiscal discipline was not maintained.

.

Israel (1985)

Israel redenominated its currency during a broader stabilization program in response to triple-digit inflation. The New Israeli Shekel (NIS) replaced the old Shekel at a ratio of 1000:1. The process was complemented by IMF-supported fiscal austerity and monetary reforms. Inflation was successfully curtailed, and investor confidence was restored.

| [29] | William Claiborne, ‘Israel to Lop 3 Zeros Off Its Shekels’ (Washington Post, 25 August 1985). |

[29]

.

Despite the pretty good practices mentioned above, currency redenomination, while often necessary for macroeconomic reform, is not without significant challenges. As noted by the Bank of Ghana, implementing redenomination policies comes with substantial costs; both financial and operational.

| [30] | Bank of Ghana, Redenomination of the Cedi. Monetary Policy (Accra, 2007). |

[30]

These include the logistical burden of rescaling financial systems, the cost of disposing of old currency notes and coins, and extensive public education and sensitization efforts required to facilitate smooth adoption. Contrary to the assumption that redenomination is a simple administrative process, PricewaterhouseCoopers highlights that businesses, in particular, face considerable transitional costs.

| [31] | PricewaterhouseCoopers, Currency Redenomination: Implications and Practical Considerations (2007). |

[31]

While some of these expenses are one-off—such as system reconfiguration or reprinting price lists; others persist until the old currency is fully withdrawn from circulation. Amoako-Agyeman and Mintah provide further insight into the social dimension of these challenges, especially in informal market settings. Their study in Ghana revealed that market women encountered difficulties adapting to the new currency.

| [32] | Francis K Amoako-Agyeman and Emmanuel K Mintah, 'The Benefits and Challenges of Ghana’s Redenomination Exercise to Market Women – A Case Study of Adum, Kejetia and Central Markets in Kumasi Metropolis' (2014) Journal of Accounting 2(1). |

[32]

Despite some eventual benefits, particularly increased efficiency in accounting and pricing, these challenges underscore the critical importance of comprehensive planning, robust stakeholder engagement, and effective public communication in implementing redenomination policies.

| [32] | Francis K Amoako-Agyeman and Emmanuel K Mintah, 'The Benefits and Challenges of Ghana’s Redenomination Exercise to Market Women – A Case Study of Adum, Kejetia and Central Markets in Kumasi Metropolis' (2014) Journal of Accounting 2(1). |

[32]

.

2.3. Beneficial Empirical Analysis of Currency Redenomination

Empirical studies across various countries provide mixed but insightful perspectives on the potential benefits of currency redenomination. A substantial body of literature identifies several potential benefits of currency redenomination, especially when implemented within a sound macroeconomic setting. Among the commonly cited advantages are: macroeconomic stabilization; enhanced safety due to reduced incidents of currency-related crime; improved ease and efficiency of transactions; time saved per exchange; cleaner and more durable currency notes; the elimination of excessive zeroes (dead weight); a reduced volume of circulating currency; and, in some cases, mitigation of inflationary pressures. These purported benefits have made redenomination an attractive policy tool for countries seeking to restore public confidence in their currency. Nevertheless, the literature reflects a divergence in outcomes, indicating that the success of redenomination is neither uniform nor automatic. For instance, Angola, Congo, and Nicaragua experienced persistent inflation despite implementing redenomination. Dogarawa argues that, beyond the immediate transitional costs imposed on governments, redenomination on its own has limited economic impact.

| [1] | Dogarawa AB, The Economics of Currency Redenomination: An Appraisal of CBN Redenomination Proposal (Ahmadu Bello University, Zaria-Nigeria 2007)

https://doi.org/10.2139/ssrn.1622144 |

[1]

Without accompanying structural reforms and credible monetary policy, the process neither halts inflation nor significantly alters public economic behaviour.

| [1] | Dogarawa AB, The Economics of Currency Redenomination: An Appraisal of CBN Redenomination Proposal (Ahmadu Bello University, Zaria-Nigeria 2007)

https://doi.org/10.2139/ssrn.1622144 |

[1]

.

Furthermore, several scholars caution that redenomination may create a false sense of monetary stability, especially where inflationary expectations remain unanchored. De Santis warns of systemic risks arising from poorly managed redenomination processes, noting that without strong institutional safeguards, redenomination may erode rather than bolster public trust.

| [17] | Roberto A De Santis, ‘A Measure of Redenomination Risk’ (Working Paper Series 1785, European Central Bank, April 2015). |

[17]

Ioana contends that redenomination has no fundamental influence on inflation, except in rare instances where price rounding effects become significant.

| [33] | Ioana D, 'The National Currency Re-Denomination Experience in Several Countries: A Comparative Analysis' (2005) International Multidisciplinary Symposium Universitaria Simpro. |

[33]

Typically, as Mosley emphasizes, the visibility of both old and new currency values helps to avoid distortions in consumer pricing and reduces the likelihood of inflationary expectations.

| [33] | Ioana D, 'The National Currency Re-Denomination Experience in Several Countries: A Comparative Analysis' (2005) International Multidisciplinary Symposium Universitaria Simpro. |

[33]

.

Lianto and Suryaputra, using structural equation modeling in Indonesia, found that citizens supported redenomination as a tool to enhance national credibility.

Similarly, Ifunanya et al. observed that redenomination can restore monetary sanity and facilitate smoother transactions through higher-value, lower-denomination currency.

| [35] | Ifunanya OC, Uchechukwu O and Chika O, 'Redenomination of Naira: A Strategy for Inflationary Reduction' (2021) International Journal of Academic Research in Business and Social Sciences 11(3) 1–15. |

[35]

Prabawani argues that while redenomination presents potential benefits such as strengthening exchange rates and improving transparency in real economic conditions, its success largely depends on strong policy understanding and preparedness among businesses in Indonesia. Evidence suggests that when businesses clearly understand redenomination policies, they are better prepared to adapt, which in turn positively influences both macroeconomic outcomes—such as price stability and exchange rate performance—and microeconomic outcomes, including simplified financial record-keeping, increased productivity, and more dynamic business activity.

| [36] | Prabawani, B. (2017). Potential impacts of redenomination: A business perspective. International Journal of Business and Society, 18(S2), 295–308. |

[36]

Pambudi et al also highlighted post-redenomination doubts among citizens regarding the government’s ability to contain hyperinflation.

| [37] | Pambudi A, Juanda B and Priyarsono DS, 'Penentu Keberhasilan Redenominasi Mata Uang: Pendekatan Historis dan Eksperimental' (2014) 17(2) Bulletin of Monetary Economics and Banking 167–196 https://doi.org/10.21098/bemp.v17i2.48 |

[37]

.

Other studies emphasize the importance of communication and political neutrality. Prabawani and Prihatini, through in-depth interviews with Indonesian industry leaders, concluded that redenomination can boost economic growth when accompanied by effective public education and devoid of political interference.

| [38] | Bulan Prabawani and Apriatni Endang Prihatini, 'Indonesian Businesses: Coping with Redenomination Policy' (2014) 8(23) Australian Journal of Basic and Applied Sciences 245–253. |

[38]

Using panel data from 164 countries between 1960 and 2015, Karnadi and Adijaya found that redenomination significantly reduced inflation and increased real Gross Domestic Product (GDP) per capita, though it had no impact on real exchange rates.

| [39] | Erwin Bramana Karnadi and Putu Rusta Adijaya, 'Redenomination: Why Is It Effective in One Country but Not in Another?' (2017) 7(3) International Journal of Economics and Financial Issues 186–195. |

[39]

.

Ullah et al. analyzed psychological impacts of redenomination across five countries (Israel, Argentina, Poland, Turkey, and Brazil), and found positive outcomes in three—Israel, Poland, and Turkey—while Argentina and Brazil experienced negative effects due to specific political and economic contexts.

| [40] | Muhammad Rizwan Ullah, Safdar Husain Tahir, Ayesha Ateeque and Iqra Shehzadi, 'How Billionaires Become Valuable Millionaires? Psychological Impact of Redenomination on Economy' (2017) 3(2) Global Journal of Economics and Business 217–228. |

[40]

In Turkey, Žídek and Chribik employed econometric techniques to conclude that redenomination directly contributed to disinflation, reinforcing its role in managing inflationary dynamics.

.

In Ghana, Obuobi et al. adopted a pre- and post-analysis of macroeconomic indicators from 1997 to 2017 and affirmed that redenomination positively impacted economic growth.

| [42] | Obuobi B, Nketiah E, Awuah F, Agyeman FO, Ofosu D, Adu-Gyamfi G, Adjei M and Amadi AG, 'Impact of Currency Redenomination on an Economy: An Evidence of Ghana' (2020) 13(2) International Business Research 62–73

https://doi.org/10.5539/ibr.v13n2p62 |

[42]

Opare-Henaku et al. found that approximately 41% of surveyed Ghanaians acknowledged the benefits of redenomination, although significant portions of the population remained either skeptical or uncertain.

| [43] | Opare-Henaku A, Mensah EC and Dzokoto VA, 'Ghanaians’ Perception and Evaluation of the New Ghana Cedi' (2013) 3(4) International Journal of Business, Humanities and Technology 1–8. |

[43]

.

Suhendra and Handayani examined the broader impact of redenomination on inflation, exchange rates, growth, and exports across 27 countries. Their findings affirm that inflation and growth are the most influenced variables, with high inflation rates often serving as a trigger for redenomination;

| [44] | Euphrasia Susy Suhendra and Sri Wayhu Handayani, 'Impacts of Redenomination on Economic Indicators' (2012) Proceedings of the International Conference on Eurasian Economies 2012, Almaty, Kazakhstan, 18–22

https://doi.org/10.36880/C03.00395 |

[44]

a view consistent with Mosley

| [2] | Mosley L, ‘Dropping Zeros, Gaining Credibility? Currency Redenomination in Developing Nations’ (Paper presented at the 2005 Annual Meeting of the American Political Science Association, 2005). |

[2]

.

In summary, cross-country experiences underscore that redenomination is not a panacea but a complementary tool contingent on the broader health of the economy. As Cohen, Caballero, Calomiris, and the IMF (supra) argue, redenomination cannot substitute for substantive reforms in fiscal policy, industrial productivity, employment generation, and trade balance.

2.4. Toward Effective Currency Redenomination and Regulatory Structures in Sierra Leone

Sierra Leone, like many other British colonized countries, has a bifurcated legal system; a legal system that hinges on dualism of operative laws cum common law and customary law.

| [45] | Vivek Maru, Between Law and Society: Paralegals and the Provision of Justice Services in Sierra Leone and Worldwide, Yale Journal of International Law 31-32 (2006). |

[45]

The country is governed by a constitutional democracy, and the foundation of its legal system is established in the Constitution of Sierra Leone 1991 (Act No. 6 of 1991), which is expressly recognized as the supreme law of the land.

The development of Sierra Leone’s legal system, unlike in jurisdictions where law evolved autonomously, has been significantly shaped by a combination of domestic and piece meal constitutional provisions and the historical influence of the English law, as formally recognized and applied through legislative and judicial basis pursuant to section 74 of the Court Act, 1965

| [46] | Courts Act, 1965 (Act No. 32 of 1965). |

[46]

through which English laws within a stipulated time frame have efficacy in the Country.

The general sources of law in the country are principally identified in Section 170 of the 1991 Constitution

| [47] | Sierra Leone Constitution of 1991 (Act No. 6 of 1991). |

[47]

and Section 74 of the Courts Act, 1965.

| [46] | Courts Act, 1965 (Act No. 32 of 1965). |

[46]

These provisions collectively establish the hierarchy and legitimacy of legal norms within the country's legal order. At the epitome of this legal order is the doctrine of parliamentary supremacy, which is constitutionally enshrined. Parliament is vested with the supreme authority to make laws, as recognized in Section 105 of the 1991 Constitution,

| [47] | Sierra Leone Constitution of 1991 (Act No. 6 of 1991). |

[47]

which confers upon Parliament the exclusive mandate to enact legislation. This legislative authority is exercised through the passage of bills, pursuant to Sections 106(1) and 106(2) of the 1991 Constitution,

| [47] | Sierra Leone Constitution of 1991 (Act No. 6 of 1991). |

[47]

which require that no bill shall become law unless it has been duly passed by Parliament and signed in accordance with the Constitution.

As a unicameral body, Sierra Leone’s Parliament operates through a single chamber, and every bill must pass through all legislative stages before it is submitted for presidential assent. While citizens may contribute to the development of legislative proposals, only Members of Parliament (MPs) or Government Ministers have the authority to formally introduce bills in Parliament—whether for Acts of Parliament, bye-laws, or subsidiary legislation.

In furtherance of parliamentary supremacy, Section 170(6) and (7) of the 1991 Constitution of Sierra Leone sets out specific requirements for the validity, publication, and enforceability of statutory instruments, orders, rules, and regulations. These provisions emphasize the need for formal enactment procedures and robust parliamentary oversight to ensure that subsidiary legislation conforms to constitutional standards and possesses legal effect.

| [47] | Sierra Leone Constitution of 1991 (Act No. 6 of 1991). |

[47]

Key among these requirements are: (i) the mandatory publication of such instruments in the Gazette within twenty-eight days of their enactment or approval—failure of which renders the instrument void from the date it was made; and (ii) the obligation to lay the instrument before Parliament, followed by publication in the Gazette. Once laid, the instrument automatically comes into effect after twenty-one days unless annulled by a two-thirds majority vote of Parliament.

It could be deliberately argued that the redenomination of Sierra Leone’s currency marked a significant economic and legal milestone. While it is submitted that the policy was publicly announced by the Bank of Sierra Leone, the legal instruments underpinning the redenomination process remained largely obscure to the general public. Thus, this section traces the legislative path toward the redenomination of currency law in Sierra Leone.

Pursuant to Section 77 of the Bank of Sierra Leone Act, 2019,

| [48] | Bank of Sierra Leone Act, 2019 (Act No. 5 of 2019). |

[48]

Parliament repealed the Bank of Sierra Leone Act, 2011 (Act No. 15 of 2011). However, all rules, regulations, notices, and other statutory instruments issued under the repealed Act remained in force and continued to have legal effect until expressly revoked or cancelled. Thus, the Bank of Sierra Leone Act, 2019 became the substantive law under which statutory instruments relating to the country’s currency redenomination were issued.

| [48] | Bank of Sierra Leone Act, 2019 (Act No. 5 of 2019). |

[48]

The Act was enacted to continue the existence of the Bank of Sierra Leone as the central monetary authority mandated to act as banker, adviser, and fiscal agent to the Government. It further empowers the Bank to support the general economic policy of the Government, maintain price stability and a sound financial system, and to formulate and implement monetary policy, financial regulations, and prudent standards.

In exercise of the powers conferred upon it under Sections 27 and 65 of the Bank of Sierra Leone Act, 2019,

| [48] | Bank of Sierra Leone Act, 2019 (Act No. 5 of 2019). |

[48]

the Bank of Sierra Leone enacted the

Redenomination of the Leone (Characteristics) Regulations, 2021 to give effect to the redenomination of the national currency. Pursuant to Regulation 1 of the said Regulations, it indicates that the existing (now defunct) currency was to be redenominated by dividing the nominal value of the old currency by a factor of one thousand (1,000), such that one thousand Leones would become one (1) Leone under the new structure.

| [49] | Redenomination of the Leone (Characteristics) Regulations, 2021. |

[49]

.

Regulations 4 and 5 of the same instrument provide for the issuance of banknotes in denominations of

One, Two, Five, Ten, and

Twenty Leones, and coins in denominations of

One, Five, Ten, Twenty-Five, and

Fifty Cents.

| [49] | Redenomination of the Leone (Characteristics) Regulations, 2021. |

[49]

The Regulations also detail the design features of both the new banknotes and coins. Immediately following the Second Schedule to the said Regulations, the Regulations are accompanied by a section titled "Memorandum of Objects and Reasons", which outlines the legal and policy rationale behind the redenomination initiative, including compliance with Section 27(4) Bank of Sierra Leone Act, 2019 (Act No. 5 of 2019) and the Bank’s broader monetary policy objectives. Worthy of reproduction is the following memorandum:

By Government Notice No. 202 published in the Sierra Leone Gazzette dated 16th August 2021, the Bank of Sierra Leone informed the general public that a new family of currency notes and coins will become legal tender in Sierra Leone in the near future.

By section 27(4) of the Bank of Sierra Leone Act the Bank shall by statutory instrument determine the characteristics of banknotes and coins issued by the bank.

It is in compliance with the aforementioned provision that the Redenomination of the Leone (Characteristics) Regulations, 2021 are issued.

| [49] | Redenomination of the Leone (Characteristics) Regulations, 2021. |

[49]

.

It is submitted that the object of the memorandum is to provide a clear legal justification for the issuance of the Redenomination of the Leone (Characteristics) Regulations, 2021, showing that the Bank of Sierra Leone acted in compliance with Section 27(4) of the Bank of Sierra Leone Act, 2019, following its public notice about the introduction of new currency notes and coins.

Pursuant to Public Notice No. 40, published by authority on the 16

th day of June 2022 in Volume CLXIII of Government Notice No. 223, it was provided that, in accordance with Regulation 1(3) of the

Redenomination of the Leone (Characteristics) Regulations, 2021, the redenominated currency would become legal tender effective 1

st July 2022. It was further stated that the existing (now defunct) currency would continue to circulate as legal tender concurrently during a transitional period.

| [50] | Redenomination of the Leone Regulations 2024. |

[50]

.

However, the conclusion of the transition period was not fixed by a single definitive date, as it was later extended on multiple occasions due to practical challenges. These included difficulties faced by individuals, institutions, and even government agencies in fully adapting to the redenominated currency. At certain points during the transition, there was a noticeable shortage of the new currency in circulation, which significantly hampered the complete withdrawal of the old notes. As a result, the date for the cessation of the legal tender status of the defunct currency was revised beyond the initial timeline indicated in the 16th June 2022 Public Notice.

Pursuant to Section 18(1) of the Redenomination of the Leone (Consequential Provisions) Regulations, 2022, now repealed in its entirety by Regulation 20 of the Redenomination of the Leone Regulations, 2024 made under the Bank of Sierra Leone Act, 2019 (Act No. 5 of 2019), the Bank of Sierra Leone issued a Public Notice formally extending the transition period for the concurrent use of the Old Leone (existing currency) and the New Leone (redenominated currency). This extension was published in Government Notice No. 40 on 16th March 2023 in The Sierra Leone Gazette, Volume CLXIV, No. 13, published by authority. Although the 2024 Regulations were enacted after the fact, they are deemed to have come into operation on 21st April 2022, thereby validating the transitional measures previously taken. The transition period, originally scheduled to end on 30th September 2022, was extended to 31st March 2023 to allow both the Old and New Leones to remain in concurrent circulation. This extension was necessitated by economic and logistical challenges affecting individuals, institutions, and the government. It provided adequate time for adjustment to the new currency regime and contributed to maintaining public confidence in the redenomination process.

Pursuant to Regulation 19 of the Redenomination of the Leone Regulations, 2024, the Bank of Sierra Leone may, by notice published in the Gazette, issue such directives and guidelines as are necessary for the better carrying out of the provisions of these Regulations. This Regulation plays a critical role in enabling the Bank of Sierra Leone to respond flexibly and effectively to the practical demands of implementing the redenomination. By empowering the Bank to issue directives and guidelines through official Gazette notices, the regulation ensures that the Bank can clarify ambiguities, address unforeseen operational challenges, and provide continuous guidance to financial institutions, businesses, and the general public. This provision supports adaptive regulation, which is essential in a complex currency transition process, where timely instructions, compliance standards, and explanatory materials are needed to sustain public confidence, ensure uniform understanding, and maintain systemic stability throughout the redenomination period.

3. Research Methodology

This study adopts a descriptive cross-sectional design to assess the implementation and consequences of the currency redenomination in Sierra Leone, with a focus on its legal, regulatory, and socio-economic dimensions. The research aims to investigate whether the timing, structural readiness, and policy coherence were sufficient to ensure a successful redenomination, as well as the extent of its benefits or failures across various sectors.

The target population for this research was limited to Sierra Leonean citizens, both at home and abroad, and non-Sierra Leonean residents currently living in Sierra Leone at the time of the redenomination exercise. This delimitation ensured that the perspectives collected were directly informed by lived experiences of the reform’s implementation, challenges, and outcomes.

The primary data source was a structured questionnaire, disseminated digitally through popular social media platforms including WhatsApp, Facebook, and Linkedin. The use of online platforms allowed for broader reach and real-time feedback, especially from respondents who may have been excluded through traditional face-to-face data collection methods due to geographical or logistical barriers.

A total of 120 respondents were targeted using simple random sampling to ensure diversity in gender, age, occupation, and regional representation. The questionnaire captured quantitative data on several key dimensions of the redenomination.

Questions were measured using a 5-point Likert scale ranging from "Strongly Agree" to "Strongly Disagree," allowing for the quantitative assessment of respondents' perceptions and experiences. To ensure validity, the questionnaire was pre-tested among a small group of Sierra Leoneans and revised based on feedback to enhance clarity and relevance.

In addition to primary data, the research draws from secondary sources and Comparative analysis with countries such as Ghana, Turkey, and Nigeria provided benchmarks for understanding the failures and missed opportunities in Sierra Leone’s case. Data was analyzed using descriptive statistics, including frequencies, percentages, and cross-tabulations, to identify trends and perceptions. The findings are presented in tables and charts for clarity and ease of interpretation.

3.1. Research Findings

This research utilized a digitally administered structured questionnaire as its principal data collection instrument, distributed through popular social media platforms such as WhatsApp, Facebook, and LinkedIn. This approach ensured broader reach among geographically dispersed Sierra Leoneans with firsthand experiences of Sierra Leone’s currency redenomination.

Out of a targeted sample of 120 respondents, the study successfully received 114 completed questionnaires, yielding a response rate of 95% which reflects a high level of engagement and participation among the intended demographic.

According to Mugenda and Mugenda, a response rate of 50% is considered adequate, 60% good, and 70% and above excellent for social research. By this standard, the response rate achieved in this study falls within the “excellent” range, indicating strong respondent cooperation and minimal non-response bias.

| [51] | Olive M. Mugenda and Abel G. Mugenda, Research Methods: Quantitative and Qualitative Approaches (African Centre for Technology Studies 2003). |

[51]

.

While 6 responses, representing 5% of the total target, were not received as anticipated, this minor shortfall does not in any way compromise the validity or reliability of the research findings. On the contrary, the high response rate enhances the empirical strength of the data and supports rigorous statistical interpretation.

To ensure methodological soundness, the data collected through the questionnaire were coded, categorized, and converted automatically into percentages using a standardized coding guide. The use of frequency distributions and cross-tabulations enabled the identification of patterns and perceptions relevant to the study’s objectives. Responses were analyzed using descriptive statistics, and findings presented in charts to facilitate clarity and comparative analysis.

3.2. General Response Information

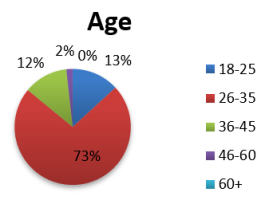

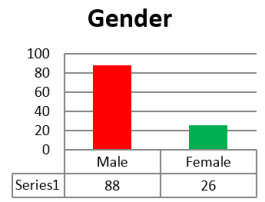

Figures 1 and 2 below present the general age and gender demographics of the 114 respondents, drawn from a targeted sample of 120; the data shows that 73% (83 respondents) fell within the age bracket of 26–35 years, 13% (15 respondents) were between 18–25 years, 12% (14 respondents) were between 36–45 years, and 2% (2 respondents) were between 46–60 years. There were no respondents above the age of 60. In terms of gender, 88 respondents (77.2%) were male, while 26 respondents (22.8%) were female.

Figure 1. Age Distribution.

Figure 2. Gender Distribution.

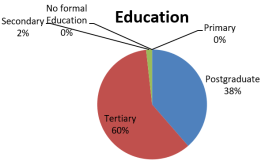

Figure 3. Educational Distribution.

Figure 3 above illustrates the educational profile of the respondents. The majority, 60%, had attained tertiary education, followed by 38% with postgraduate qualifications, and 2% with secondary education. There were no respondents with only primary education or non-formal education.

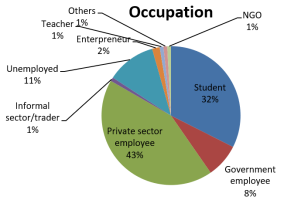

Figure 4. Occupational Distribution.

Figure 4 above illustrates the occupational distribution of the 114 respondents. Of these, 43% were employed in the private sector, 8% worked in government, and 32% were students. Additionally, 1% each were in the informal sector/trading, unemployed, teaching, or employed by a non-governmental organization (NGO), while 2% were entrepreneurs and 1% reported other occupations. As the survey was conducted online, it reached participants from across all regions of Sierra Leone.

3.3. Knowledge and Awareness

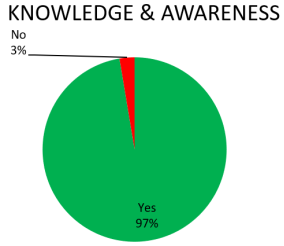

Figure 5. Occupational Distribution.

Figure 5 above illustrates respondents’ knowledge and awareness of the recent currency redenomination in Sierra Leone and the law governing its implementation; based on their responses to the question:

“Are you aware that Sierra Leone recently redenominated its currency?” Out of the 114 respondents, 97% (110 participants) answered “Yes,” indicating they were aware, while 3% (4 participants) responded “No,” indicating they were not aware.

When asked how they first heard about the currency redenomination, half of the respondents (50%) cited social media as their primary source of information, followed by government communication (22.8%) and radio (12.3%). Smaller proportions indicated television (5.6%), family or friends (7%), stakeholder engagement (1.8%), and WhatsApp (0.9%).

In terms of understanding, the majority (69.3%) correctly associated currency redenomination with “removing zeros” from the currency, while 24.6% described it as “changing currency value,” 5.3% believed it meant “replacing the currency name,” and 0.9% admitted they did not know.

Respondents were also asked to rate how well-informed they felt about the redenomination process on a scale of 1 (least informed) to 5 (most informed). The ratings were distributed as follows: 12 respondents selected 1, 28 selected 2, 35 selected 3, 22 selected 4, and 17 selected 5.

When asked whether the public was adequately sensitized about the redenomination, 63.2% (72 respondents) answered “No,” 16.7% (19 respondents) answered “Yes,” and 20.2% (23 respondents) responded “Maybe.”

3.4. Impact and Experience with the Currency Redenomination

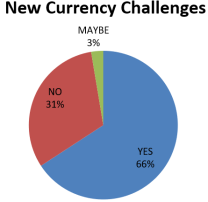

Figure 6. Currency Challenge.

Regarding the impact and experience of the currency redenomination, respondents were asked whether they had personally encountered any challenges using the new Leones. A majority, 66% (75 respondents), reported that they had experienced challenges, while 31% (36 respondents) stated they had not, and 3% (3 respondents) were uncertain. The challenges experienced by respondents using the new Leones were varied and multifaceted. Common issues included merchants refusing to accept old notes when the policy was initially implemented, limited availability of new currency notes, and confusion over pricing, and difficulties in calculating change.

When asked whether the currency redenomination affected prices of goods and services, respondents expressed mixed views. A notable portion believed prices increased (44 respondents), while only a few thought prices decreased (4 respondents). 30 respondents reported no change in prices, and 36 were unsure.

Regarding the impact of redenomination on daily transactions, responses were almost evenly split: 40 respondents felt that transactions had become easier, 39 disagreed, 34 were uncertain, and 1 respondent indicated that the redenomination had not made transactions easier but had instead caused them to spend more.

3.5. Trust and Governance

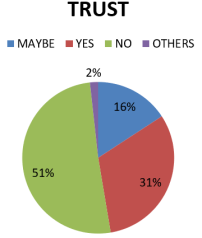

This section examined respondents’ trust in the currency redenomination in Sierra Leone. The findings reveal that a majority, 51%, expressed no trust in the redenomination process, while 31% indicated that they did have trust. Additionally, 16% were unsure about their level of trust, and 2% fell into other unspecified categories.

Figure 7. Redenomination Trust.

Respondents were asked their opinion on the necessity of the redenomination, with the majority, 60, stating it was not necessary, 33 believing it was necessary, 16 indicating maybe, and 5 selecting other responses. When rating the transparency of the redenomination process, only 10 respondents considered it very transparent, 33 somewhat transparent, while a majority of 58 believed it was not transparent. Additionally, 15 were unsure, and 1 respondent felt the process lacked transparency in all aspects. Regarding community consultation, most respondents (101) reported that they were not consulted or informed in any community meetings about the redenomination, with only 13 saying they had been. Finally, when asked about parliamentary oversight of the process, 96 respondents felt that Parliament did not provide sufficient oversight, 13 believed it did, and 5 gave other or uncertain responses.

3.6. Coins and Transaction Experience

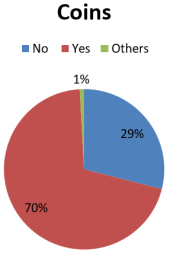

This component focused on respondents’ transaction experiences following the implementation of the Redenomination of the Leone (Characteristics) Regulations, 2021, which give legal effect to the redenomination of Sierra Leone’s national currency. Regulations 4 and 5 of this instrument specify the issuance of new banknotes in denominations of One, Two, Five, Ten, and Twenty Leones, alongside coins in denominations of One, Five, Ten, Twenty-Five, and Fifty Cents. In this context, participants were asked about their awareness of the inclusion of coins in the redenominated currency and their related transaction experiences. When asked whether they were aware that coins were to be part of the redenominated currency, 70% responded “Yes,” 29% said “No,” and 1% was unsure.

Figure 8. Redenominated Coins.

Further questions under this component explored respondents’ actual experience with coins since the redenomination took effect. When asked if they had seen or used any coins, a majority of 101 respondents indicated “No,” while only 12 reported having used coins, and 1 respondent gave another response. Regarding the impact of the absence of coins on day-to-day transactions, common difficulties included unfair rounding up of prices (63 respondents) and challenges in receiving accurate change (28 respondents). Some respondents (10) felt forced to accept goods instead of receiving proper change, while 12 reported no impact, and 1 provided other responses.

When asked whether the use of coins would improve small-scale transactions in markets, shops, or transportation, 101 respondents agreed it would, while 13 disagreed. Similarly, a strong majority of 102 respondents preferred the introduction of coins to complement the redenominated banknotes, with only 9 opposed and 3 giving other responses.

3.7. Respondent Recommendations & Expectations

Under this component in the public survey, participants were given the opportunity to share their recommendations and expectations regarding future financial reforms. The most frequently suggested improvement was to ensure wider public consultation before major economic decisions are made, highlighted by 44 respondents. Increasing nationwide sensitization through radio, television, and local languages was also emphasized by 14 participants. 13 respondents recommended the introduction of coins as part of the redenominated currency to facilitate small transactions, while 29 called for the establishment of proper price control mechanisms to curb inflation. 12 respondents urged for greater transparency and inclusivity in the reform process, and others suggested training market sellers.

When asked if future currency changes should involve more public consultation, an overwhelming majority of 112 respondents agreed, with only 2 dissenting. Furthermore, 105 respondents expressed the view that redenomination alone cannot resolve economic problems, with only 9 believing it could. Similarly, 112 respondents indicated a desire to receive more education on national economic reforms, reflecting a strong appetite for increased public awareness and understanding.

The final comments section captured a wide range of opinions reflecting both frustration and cautious optimism. Several respondents criticized the redenomination as untimely, ineffective, or primarily cosmetic, highlighting that removing zeros did little to address underlying economic challenges such as inflation, currency depreciation, and the rising cost of living. Comments underscored a perceived lack of transparency and inadequate public consultation throughout the process. Many called for comprehensive economic reforms, including effective inflation control, stronger financial management, and better engagement with all stakeholders prior to implementing such policies.

On the other hand, some respondents noted that while the redenomination improved cash handling and comparability of the Leone to other currencies, it failed to stabilize the economy or improve purchasing power. The absence of coins was repeatedly mentioned as a practical impediment to everyday transactions, with calls for their introduction to complement banknotes. Others suggested exploring a cashless society or maintaining existing denominations while introducing higher value notes.

Conclusively, respondents emphasized the need for transparent, inclusive, and well-communicated reforms supported by robust macroeconomic policies to ensure lasting economic stability.

5. Conclusion

This article, A Nation Gone Wrong: Currency Redenomination Law and Regulatory Failure in Sierra Leone, intentionally frames a paradox: its title evokes systemic collapse, yet the empirical record assembled herein reveals a more ambivalent verdict, one of formal legality and technical execution, coupled with substantive shortfalls in governance, implementation and macroeconomic impact. It is submitted that the Bank of Sierra Leone having lawfully effected the redenomination, through the Bank of Sierra Leone Act, 2019 and the Redenomination Regulations (2021), and other legal architecture for transition (including transitional extensions published in the Gazette), remains short serviced with implementation beyond what obtains in the legal instruments.

Notwithstanding that formal legitimacy, the primary data show important and persistent deficits in the reform’s substance. The study’s high response rate (95%) and respondent profile (predominantly young, educated, and digitally reachable) confer empirical weight to the perceptions captured: widespread awareness of the change but limited depth of understanding and a pronounced trust deficit. These findings are material because they reveal a policy that was visible yet not sufficiently comprehensible or legitimate in the eyes of most citizens; a condition inimical to the social licence necessary for monetary reform.

Implementation lacunae are particularly salient in the practical domain. Although the Regulations expressly provided for coin denominations, coins have scarcely circulated and market participants report routine rounding abuses and transactional friction; failures that convert a legal instrument into a hollow promise on the ground. This implementation gap is not merely operational; it has distributive and legal consequences (regressive rounding, erosion of purchasing power for the poor, and market distortions) that undermine the redenomination’s asserted benefits.

Macro-level indicators and public perceptions likewise requires caution: inflationary pressures persisted after redenomination, a result consistent with World Bank analysis that attributes recent inflation to external shocks and expansionary fiscal/monetary stances rather than to redenomination per se. Put differently, the reform altered nominal units without materially altering the structural drivers of price instability.

In view of the foregoing analysis, as read against the comparative literature, as well as the article’s own normative exposition on regulatory governance, the reasonable legal–economic judgment is that Sierra Leone’s currency redenomination constitutes progress in form but a deficiency in substance; an executed statutory regimen that has not yet been embedded within the institutional, fiscal, and communicative platforms required to secure enduring macroeconomic stability or equitable distributive gains. When all is said and done, the proof of the pudding, they say, is in the eating; and the true measure of the reform should not be found in the pages of the Gazette or the precision of its enabling instruments alone, but in the economic realities of the citizens it was intended to serve.

Recommendation

These recommendations focus on law and public policy to help fix the governance, process, and economic problems found in the research.

1) Parliamentary Oversight: Parliament should actively exercise its oversight role over the Bank of Sierra Leone quarterly concerning the monitoring of the currency redenomination so as to enhance government accountability and strengthen public trust.

2) Revamp Public Education: The Bank of Sierra Leone should revamp public education program on the redenominated currency to ensure widespread understanding, trust and confidence among all citizens to understand that redenomination alone does not solve the economic deficiencies in the country.

3) Include Redenomination in a Broader Economic Stability Plan: Adjust government spending and borrowing plans to control inflation and work with international partners like the IMF for expert help to make reform a part of a longer public policy plan.

4) Make Coin Issuance a Priority: The Bank of Sierra Leone should introduce coins to ease transactions especially for people in informal sector as a means to end price rounding and distortion.

5) Set Up a Price Monitoring Unit: The Bank of Sierra Leone should create a new unit by law that watches prices, investigates unfair rounding, publishes monthly price reports on essential goods.

6) Start an Implementation Review: The Bank of Sierra Leone should establish an independent review to assess the effects redenomination on inflation, transaction times, currency availability, public trust, and the impact on vulnerable groups.

7) Enhance Economic Production and Export Policies: Implement policies that strengthen Sierra Leone’s production capacity and promote increased exports to boost overall economic growth, recognizing that redenomination alone cannot end inflation.

8) Strengthen Foreign Exchange Management: Develop and enforce policies that stabilize foreign exchange markets in support of the redenominated currency and ensure consistent exchange rates by reducing volatility, thereby fostering economic confidence and stability.

9) Strengthen Banking Sector Regulation and Salone Payment Switch Integration: Implement robust regulatory measures to ensure the smooth operation of Sierra Leone’s banking sector and the integration of the Salone Payment Switch to enhance transaction efficiency as critical components for successful currency redenomination and economic stability.