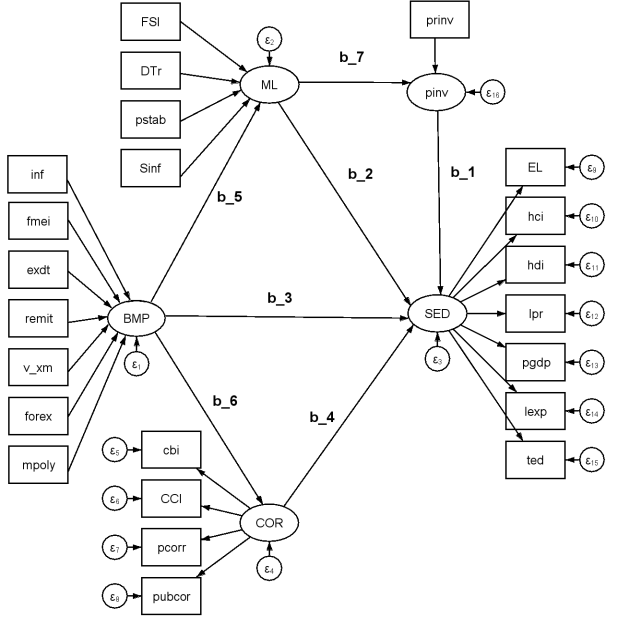

The intricacies surrounding the measurement and modelling of money laundering (ML), corruption (COR), and black-market prevalence (BMP), as well as their effects on socio-economic development (SD), introduce significant challenges to accurately capturing and understanding these phenomena. There is a plethora of theories on individual measurements of each concept, but regrettably, they are not immune to criticism, and no such explicit approach is available to study the nexus between these complex concepts. The current study employs the multiple indicator approach to measure ML, COR, and SD, and utilizes the PLS-SEM approach to explore the relationships between these complex concepts, with a focus on the mediating role of the BMP. The per capita investment (PCI) expenditures, modelled through the multiple indicator approach, have been used as the control variables. The study has adopted a data-driven approach to conduct pre- and post-estimation analysis for the constructs and validate the results for a cross-section of 198 countries in 2022. The results indicate that the impact of corruption on socio-economic development is negative and statistically significant. The black market has a direct, negative, and significant impact on socio-economic development; similarly, the BMP has a positive and significant effect on ML. In addition to the direct impact on socio-economic development, BMP also indirectly affects SED through the ML. The direct effects of ML on SED are adverse, while it has an indirect positive impact on SED through its significant multiplier effect on per capita investment. These findings have implications for anti-money laundering and anti-corruption policies worldwide.

| Published in | Research & Development (Volume 7, Issue 1) |

| DOI | 10.11648/j.rd.20260701.11 |

| Page(s) | 1-23 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

PLS-SEM, Money Laundering, Black Market, Socio-economic Development, Corruption

BMP | COR | SED | ML | NR | pinv | |

|---|---|---|---|---|---|---|

bmp_1 | 0.756 | |||||

bmp_2 | 0.634 | |||||

bmp_3 | 0.625 | |||||

bmp_4 | 0.786 | |||||

bmp_5 | 0.698 | |||||

bmp_6 | 0.763 | |||||

bmp_7 | 0.612 | |||||

cor_1 | 0.754 | |||||

cor_2 | 0.783 | |||||

cor_3 | 0.658 | |||||

cor_4 | 0.693 | |||||

sed_1 | 0.698 | |||||

sed_2 | 0.664 | |||||

sed_3 | 0.711 | |||||

sed_4 | 0.738 | |||||

sed_5 | 0.692 | |||||

sed_6 | 0.778 | |||||

sed_7 | 0.891 | |||||

ml_1 | 0.758 | |||||

ml_2 | 0.772 | |||||

ml_3 | 0.823 | |||||

ml_4 | 0.730 | |||||

pinv | 1.000 |

alpha | rhoC | AVE | rhoA | |

|---|---|---|---|---|

COR | 0.884 | 0.784 | 0.794 | 0.686 |

BMP | 0.794 | 0.841 | 0.885 | 0.586 |

ML | 0.858 | 0.892 | 0.698 | 0.754 |

pinv | 1 | 1 | 1 | 1 |

SED | 0.771 | 0.882 | 0.893 | 0.722 |

COR | BMP | ML | NR | pinv | SED | |

|---|---|---|---|---|---|---|

COR | 0.891 | |||||

BMP | 0.635 | 0.941 | ||||

ML | 0.737 | 0.650 | 0.835 | |||

pinv | 0.599 | 0.651 | 0.647 | 0.492 | 1 | |

SED | 0.621 | 0.679 | 0.759 | 0.505 | 0.684 | 0.945 |

Original Est. | Bootstrap Mean | Bootstrap SD | T Stat. | 2.5% CI | 97.5%CI | |

|---|---|---|---|---|---|---|

COR -> SED | 0.7846 | 0.7818 | 0.1764 | 4.4481 | 1.1275 | 0.4361 |

BMP -> ML | 0.8502 | 0.8539 | 0.2494 | 5.4148 | 1.3426 | 0.3652 |

BMP -> Cor | 0.7174 | 0.7195 | 0.0979 | 3.2017 | 0.9114 | 0.5276 |

BMP -> ML | 0.9223 | 0.9281 | 0.0998 | 3.0709 | 1.1237 | 0.7324 |

BMP -> SED | 0.9084 | 0.9034 | 0.1179 | 7.7016 | 1.1346 | 0.6722 |

ML -> pinv | 0.9080 | 0.9100 | 0.1824 | 2.7858 | 1.2674 | 0.5526 |

ML -> SED | 0.9368 | 0.9319 | 0.2429 | 4.2680 | 1.4080 | 0.4558 |

pinv -> SED | 0.8782 | 0.8108 | 0.0918 | 3.0302 | 0.9907 | 0.6308 |

LV | Indicator | VIF | LV | Indicator | VIF |

|---|---|---|---|---|---|

COR | Cor_1 | 1.019 | ML | ml_1 | 1.020 |

Cor_2 | 1.020 | ml_2 | 1.007 | ||

Cor_3 | 1.025 | ml_3 | 1.004 | ||

Cor_4 | 1.026 | ml_4 | 1.021 | ||

BMP | bmp_1 | 1.031 | SED | Sed_1 | 1.080 |

bmp_2 | 1.054 | Sed_2 | 1.060 | ||

bmp_3 | 1.032 | Sed_3 | 1.049 | ||

bmp_4 | 1.031 | Sed_4 | 1.076 | ||

bmp_5 | 1.022 | Sed_5 | 1.048 | ||

bmp_6 | 1.037 | Sed_6 | 1.028 | ||

bmp_7 | 1.024 | Sed_7 | 1.050 |

Original Est. | Bootstrap Mean | Bootstrap SD | T Stat. | 2.5% CI | 97.5% CI | |

|---|---|---|---|---|---|---|

bmp_1 -> BMP | 0.209 | 0.198 | 0.062 | 3.210 | 0.163 | 0.840 |

bmp_2 -> BMP | 0.063 | 0.067 | 0.020 | 3.384 | 0.692 | 0.048 |

bmp_3 -> BMP | 0.151 | 0.150 | 0.035 | 4.282 | 0.445 | 0.017 |

bmp_4 -> BMP | 0.006 | 0.005 | 0.001 | 3.230 | 0.001 | 0.770 |

bmp_5 -> BMP | 0.151 | 0.150 | 0.044 | 3.440 | 0.102 | 0.812 |

bmp_6 -> BMP | 0.345 | 0.344 | 0.279 | 1.234 | -0.492 | 0.568 |

bmp_7 -> BMP | 0.123 | 0.122 | 0.031 | 3.919 | 0.677 | 0.109 |

cor_1 -> COR | 0.442 | 0.441 | 0.097 | 4.567 | 0.440 | 0.932 |

cor_2 -> COR | 0.149 | 0.148 | 0.035 | 4.196 | 0.107 | 0.845 |

cor_3 -> COR | 0.349 | 0.348 | 0.082 | 4.265 | 0.340 | 0.886 |

cor_4 -> COR | 0.194 | 0.193 | 0.036 | 5.280 | 0.431 | 0.009 |

sed_1 -> SED | 0.342 | 0.341 | 0.033 | 10.404 | 0.508 | 0.031 |

sed_2 -> SED | 0.486 | 0.485 | 0.266 | 1.822 | -0.336 | 0.636 |

sed_3 -> SED | 0.084 | 0.083 | 0.263 | 0.314 | -0.441 | 0.532 |

sed_4 -> SED | 0.463 | 0.462 | 0.284 | 1.625 | -0.457 | 0.602 |

sed_5 -> SED | 0.460 | 0.459 | 0.044 | 10.333 | 0.751 | 0.107 |

sed_6 -> SED | 0.638 | 0.637 | 0.100 | 6.374 | 0.568 | 0.608 |

sed_7 -> SED | 0.437 | 0.436 | 0.100 | 4.377 | 0.463 | 0.016 |

ml_1 -> ML | 0.356 | 0.355 | 0.075 | 4.738 | 0.719 | 0.327 |

ml_2 -> ML | 0.383 | 0.382 | 0.441 | 0.867 | -0.642 | 0.932 |

ml_3 -> ML | 0.412 | 0.411 | 0.099 | 4.142 | 0.447 | 0.011 |

ml_4 -> ML | 0.330 | 0.329 | 0.049 | 6.774 | 0.716 | 0.100 |

pinv -> pinv | 1 | 1 | - | - | - | - |

Endo-Latent <- | Exo- Latent | VIF |

|---|---|---|

SED <- | <- COR | 3.038 |

<- ML | 5.102 | |

<- NR | 4.027 | |

<-PINV | 1.075 | |

ML<- | <- COR | 1.001 |

<- BMP | 1.001 |

Original Est. | Bootstrap Mean | Bootstrap SD | T Stat. | 2.5% CI | 97.5% CI | |

|---|---|---|---|---|---|---|

COR -> SED | -0.297 | -0.297 | 0.218 | -1.362 | -0.404 | 0.365 |

BMP -> ML | 0.255 | 0.256 | 0.109 | 2.336 | 0.503 | 0.544 |

ML -> pinv | 0.247 | 0.248 | 0.087 | 2.831 | 0.195 | 0.459 |

ML -> SED | -0.097 | -0.097 | 0.022 | -4.306 | 0.399 | 0.376 |

BM -> COR | 0.100 | 0.100 | 0.035 | 2.857 | 0.237 | 0.270 |

BM -> SED | 0.087 | 0.087 | 0.034 | 2.521 | 0.301 | 0.241 |

pinv -> SED | 0.165 | 0.165 | 0.063 | 2.621 | 0.240 | 0.394 |

Original Est. | Bootstrap Mean | Bootstrap SD | T Stat. | 2.5% CI | 97.5% CI | |

|---|---|---|---|---|---|---|

COR -> SED | -0.2967 | 0.2966 | 0.2181 | 1.3623 | -0.4121 | 0.3641 |

BMP -> ML | 0.2554 | 0.2553 | 0.0594 | 4.2978 | 0.5027 | 0.5442 |

BMP -> pinv | 0.0632 | 0.0631 | 0.0108 | 5.8454 | 0.1350 | 0.1393 |

BMP -> SED | 0.0105 | 0.0104 | 0.0770 | 0.1344 | -0.1340 | 0.1480 |

ML -> pinv | 0.2474 | 0.2473 | 0.0874 | 2.8290 | 0.1953 | 0.4592 |

ML -> SED | -0.0966 | -0.0965 | 0.0234 | -4.1282 | 0.3916 | 0.3863 |

ML -> SED | 0.0364 | 0.0363 | 0.0102 | 3.6301 | 0.0325 | 0.3284 |

pinv -> SED | 0.1654 | 0.1653 | 0.0531 | 3.1101 | 0.2396 | 0.3937 |

PLS-SEM | Partial Least Squares Structural Equation Modelling |

AML | Anti Money Laundering |

SED | Socio-Economic Development |

BMP | Black Market Prevalence |

ML | Money Laundering |

Corr | Corruption |

CI | Confidence Interval |

HTMT | Hetero-Trait-Mono-Trait |

AVE | Average Variance Extracted |

VIF | Variance Inflating Factor |

cSEM | Covariance Based Structural Equation Modeling |

SEMinR | Structural Equation Modeling Using R |

WBG | World Bank Group |

Sr# | LV | indicator Name | Label | Definition | Source |

|---|---|---|---|---|---|

1 | Corruption (Corr) | Bayesian Corruption Index | BCI | The BCI is an index of the perception of overall corruption (abuse of public power for private gain) within a country. It is constructed from the methodological skeleton of the WBGI and CPI, using 17 different surveys of countries' inhabitants, business executives, and governments. | Quality of Government Datasets bci_bci |

2 | Control of Corruption Index | CC | Published by the WBG and maintained by Daniel Kaufman, the team updated it in 2023. This measure of the Control of Corruption captures perceptions of the extent to which public power is exercised for private gain, including petty and grand forms of corruption and the "capture" of the state by elites and private interests. | World bank | |

3 | Political corruption Index | Pol_corr | How pervasive is political corruption | Quality of Government Datasets (QoG) | |

4 | Public sector corruption | Pubs_corr | Transparency, accountability, and corruption in the public sector rating (1=low to 6=high), World Bank Group (WBG) CPIA database. | WBG CPIA database | |

5 | Money Laundering (ML) | Drugs trafficking | Drugs | the amount of drug (in kilogram) discovered per 100,000 people | UNODC |

6 | Political Stability and Terrorism | polst | Political Stability and Absence of Violence/Terrorism measures perceptions of the likelihood of political instability and/or politically motivated violence, including terrorism. Estimate gives the country's score on the aggregate indicator in units of standard normal distribution, i.e., ranging from approximately -2.5 to 2.5. | WDI | |

7 | size of the informal economy | infesize | The World Bank database of the informal economy. The MIMIC-based estimates of the informal output (% official GDP). | WBG datasets | |

8 | Financial secrecy index | FSI | The Financial Secrecy Index ranks the jurisdictions most complicit in helping individuals hide their finances from the rule of law. | justice network & global policy organization | |

9 | Socio-economic Development (SED) | Human Capital Index | (HCI) | The Human Capital Index (HCI) combines health and education indicators into a measure of the human capital that a child born today can expect to obtain by their 18th birthday on a scale from 0 to 1. Higher values indicate higher expected human capital measured by the World Bank. | WDI/ WBG |

10 | tertiary education/students enrolled over ten years | tert_edu | The ratio of students enrolled in tertiary education to the population over ten years of age (tert_edu) is calculated from the WDI. | WDI/ WBG | |

11 | Human Development Index | (HDI) | Extracted from the World Bank database as an overall proxy for the development in three dimensions of development (health, education, and standard of living). | UNDP/ WDI | |

12 | life expectancy | lifexp | Life expectancy at birth in years was calculated from the World Development database. | WDI | |

13 | % pop Access to electricity | acc_elec | This is based on national surveys and the World Bank's electrification database. The electrification data are collected from industry, national surveys, and international sources. This is included to account for the technological development and the standard of living of rural households. | Industries. National surveys | |

14 | Per capita GDP | GDP_cap | Gross domestic product per capita (GDP_capita) accounts for economic development in the real term. | WDI | |

15 | fem/male labor force participation rate | lb_fem_m | ratio of female to male labor force participation | WDI | |

16 | Private Expenditures per capita | per capita private expenditures | (Prexcap) | this is the sum of final consumption expenditures plus the private investment divided by the total population | WDI |

17 | Natural resource dependence | Average of oil rents % GDP and Agriculture, forestry, and fishing, value added (% of GDP) | c_aggdp | ½ [share of oil rents % gdp+ Agriculture, forestry, and fishing, value added (% of GDP)] | WDI |

18 | Black Market Prevalence BMP | inflation | inf | Measured by the CPI Annual % age from the world development indicators. | WDI |

19 | Financial markets efficiency index | FMEI | percentage gap between official and black-market exchange rate | IMF Database with the indicator code FD_FME_IX | |

20 | External Debt | edt | total external debt as a percentage of GDP | WDI | |

21 | remittances | remit | remittances received as a percentage of GDP | WDI | |

22 | Real effective exchange rate | v_xm | The real effective exchange rate is the nominal effective exchange rate (a measure of the value of a currency against a weighted average of several foreign currencies) divided by a price deflator or index of costs. | WDI | |

23 | Foreign Exchange Reserves | Forex | Total reserves are a percentage of total external debt. The data is obtained from the WDI against the FI data code.RES.TOTL.DT.ZS. | WDI | |

24 | Broad Money (%GDP) | M_Policy | Broad money (IFS line 35L..ZK) is the sum of currency outside banks; demand deposits other than those of the central government; the time, savings, and foreign currency deposits of resident sectors other than the central government; bank and traveler’s checks; and other securities such as certificates of deposit and commercial paper. | IFS |

| [1] | Acemoglu, D., & Robinson, J. A. (2010). Why is Africa poor? Economic history of developing regions, 25(1), 21-50. |

| [2] | Aidt, T. S. (2003). Economic analysis of corruption: a survey. The Economic Journal, 113(491), F632-F652. |

| [3] | Aidt, T., Dutta, J., & Sena, V. (2008). Governance regimes, corruption, and growth: Theory and evidence. Journal of Comparative Economics, 36(2), 195-220. |

| [4] | Alesina, A., & Weder, B. (2002). Do corrupt governments receive less foreign aid?. American Economic Review, 92(4), 1126-1137. |

| [5] | Andersson S. (2017). Beyond Unidimensional Measurement of Corruption. Public Integrity, 19(1): 58- 76. |

| [6] | Bartlett, B. L. (2002). The negative effects of money laundering on economic development. Platypus Magazine, (77), 18-23. |

| [7] | Biles, J. J. (2009). Informal work in Latin America: Competing perspectives and recent debates. Geography Compass, 3(1), 214-236. |

| [8] | Boeschoten, W. C. and M. M. G. Fase (1984), The Volume of Payments and the Informal Economy in the Netherlands 1965–1982. M. Nijhoff, Dordrecht. |

| [9] | Bollen, K. A. (1989). Structural equations with latent variables (Vol. 210). John Wiley & Sons. |

| [10] | Bollen, K., & Lennox, R. (1991). Conventional wisdom on measurement: A structural equation perspective. Psychological bulletin, 110(2), 305. |

| [11] | Cao, Y., Fan, M. Y., Hlatshwayo, S., Petrescu, M., & Zhan, Z. (2021). A sentiment-enhanced corruption perception index. International Monetary Fund. |

| [12] | Chang, C. P., & Hao, Y. (2017). Environmental performance, corruption, and economic growth: global evidence using a new data set. Applied Economics, 49(5), 498-514. |

| [13] | Cieślik, A., & Goczek, Ł. (2018). Control of corruption, international investment, and economic growth–Evidence from panel data. World Development, 103, 323-335. |

| [14] | Contini, B. (1981), Labor market segmentation and the development of the parallel economy: the Italian experience, Oxford Economic Papers, 33, pp. 401–412. |

| [15] | D'Agostino, G., Dunne, J. P., & Pieroni, L. (2016). Corruption and growth in Africa. European Journal of Political Economy, 43, 71-88. |

| [16] | Daniel, J. (2016). Advisory Statement for Effective International Practice: Combatting Corruption and Enhancing Integrity: A Contemporary Challenge for the Quality and Credibility of Higher Education. Council for Higher Education Accreditation. |

| [17] | Del Boca, D., & Forte, F. (1982). Recent empirical surveys and theoretical interpretations of the parallel economy in Italy. The underground economy in the United States and abroad, Lexington (Mass.), Lexington, 160- 178. |

| [18] | Dell’Anno R (2020a) Corruption worldwide: an analysis by partial least squares structural equation modeling. Public Choice 184(3): 327–350. |

| [19] | Dell’Anno, R., & Maddah, M. (2023). Money laundering, corruption, and socioeconomic development in Iran: an analysis by structural equation modeling. International Review of Economics, 70(3), 395-417. |

| [20] | Dijkstra, T. K., & Henseler, J. (2015a). Consistent and asymptotically normal PLS estimators for linear structural equations. Computational Statistics & Data Analysis, 81, 10–23. |

| [21] | Dijkstra, T. K., & Henseler, J. (2015b). Consistent partial least squares path modeling. MIS Quarterly, 39(2), 297–316. |

| [22] | Dimant, E., & Tosato, G. (2018). Causes and effects of corruption: what has the past decade's empirical research taught us? A survey. Journal of economic surveys, 32(2), 335-356. |

| [23] | Dincer, O., & Johnston, M. (2019). Black and (thin) blue (line): Corruption and other political determinants of police killings in America. Governance, 36(1), 167-186. |

| [24] | Donchev, D., & Ujhelyi, G. (2014). What Do Corruption Indices Measure? Economics & Politics, 26(2), 309–331. |

| [25] | Enste, D., & Heldman, C. (2017). Causes and consequences of corruption: An overview of empirical results. |

| [26] | Farzanegan, M. R., & Witthuhn, S. (2017). Corruption and political stability: Does the youth bulge matter?. European Journal of Political Economy, 49, 47-70. |

| [27] | Feige, E. L. (1996). Overseas holdings of US currency and the underground economy. Exploring the Underground Economy. Kalamazoo, Michigan, 5-62. |

| [28] | Feige, E. L. (2016). Professor Schneider's shadow economy: what do we really know? A rejoinder. Forthcoming in the Journal of Tax Administration, 2(2). |

| [29] | Feige, E. L. (2016). Reflections on the Meaning and Measurement of Unobserved Economics. |

| [30] | Fornell, C., Bookstein, F. L.:(1982). Two structural equation models, LISREL and PLS, applied to consumer choice theory. J. Mark. Res. 19(4), 440–452 (1982). |

| [31] | Fortin, B., Garneau, G., Lacroix, G., Lemieux, T. and Montmarquette, C. (1996), L’Economie Souterraine au Quebec: mythes et realites, Presses de l’Universite Laval, Laval. |

| [32] | Frey, B. S. and H. Weck (1983a), Bureaucracy and the shadow economy: a macro-approach, in Hanusch, H. (ed.), Anatomy of Government Deficiencies, Springer, Berlin, pp. 89–109. |

| [33] | Frey, B. S. and H. Weck-Hannemann (1984), The hidden economy as an “unobserved” variable, European Economic Review, 26, pp. 33–53. |

| [34] | Global Financial Integrity (2019), Illicit Financial Flows to and from Developing Countries, 2006-2015, Washington, DC: April. |

| [35] | Gnutzmann, H., McCarthy, K. J., & Unger, B. (2010). Dancing with the devil, Country size, and the incentive to tolerate money laundering. International Review of Law and Economics, 30(3), 244-252. |

| [36] | Goel, R. K., & Nelson, M. A. (2010). Causes of corruption: History, geography, and government. Journal of Policy Modeling, 32(4), 433-447. |

| [37] | Gründler, K., & Potrafke, N. (2019). Corruption and economic growth: New empirical evidence. European Journal of Political Economy, 60, 101810. |

| [38] | Habib, M., & Zurawicki, L. (2002). Corruption and foreign direct investment. Journal of International. |

| [39] | Havranek, T., Horvath, R., & Zeynalov, A. (2016). Natural resources and economic growth: A meta-analysis. World Development, 88, 134-151. |

| [40] | Henry, L., & Moses, S. (2020). The impact of money laundering in beautiful places: The case of Trinidad and Tobago. Journal of Economics and International Finance, 12(1), 39-47. |

| [41] | Huang, C. J. (2016). Is corruption bad for economic growth? Evidence from Asia-Pacific countries. The North American Journal of Economics and Finance, 35, 247-256. |

| [42] | Hua, G. B. (2005). IT barometer 2003: Survey of the Singapore construction industry and a comparison of results. J. Inf. Technol. Constr., 10, 1-13. |

| [43] | Johnson, S., Kaufmann D. and P. Zoido-Lobatón (1998b), Corruption, Public Finances and the Unofficial Economy, World Bank Policy Research Working Paper Series No. 2169, The World Bank, Washington, D.C. |

| [44] | Hair, J. F., Astrachan, C. B., Moisescu, O. I., Radomir, L., Sarstedt, M., Vaithilingam, S., & Ringle, C. M. (2021). Executing and interpreting applications of PLS-SEM: Updates for family business researchers. Journal of Family Business Strategy, 12(3), 100392. |

| [45] | Kalioberda, A., & Kaufmann, D. (1996). Integrating the unofficial economy into the dynamics of post-socialist economies: A framework of analysis and evidence. The World Bank. 015 p 5. |

| [46] | La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. (1999). The quality of government. Journal of Law, Economics, and Organization, 15(1), 222-279. |

| [47] | Lambsdroff, J. G. (2007). The institutional economics of corruption and reform: Theory, evidence, and policy. Cambridge University Press. |

| [48] | Leonard, M. (2000). Coping strategies in developed and developing societies: the workings of the informal economy. Journal of International Development: The Journal of the Development Studies Association, 12(8), 1069-1085. |

| [49] | Loayza, N., Villa, E., & Misas, M. (2019). Illicit activity and money laundering from an economic growth perspective: A model and an application to Colombia. Journal of Economic Behavior & Organization, 159, 442-487. |

| [50] | Lohmöller, J. B. (2013). Latent variable path modeling with partial least squares. Springer Science & Business Media. |

| [51] | Markovska, A., & Adams, N. (2015). Political corruption and money laundering: lessons from Nigeria. Journal of Money Laundering Control, 18(2), 169-181. |

| [52] | Masciandaro, D. (1999). Money laundering: the economics of regulation. European Journal of Law and Economics, 7, 225-240. |

| [53] | Masciandaro, D. (2007). Economics of money laundering: A primer. Paolo Baffi Centre Bocconi University Working Paper, (171). |

| [54] | McCrohan, K., Smith, J. D. and Adams, T. K. (1991), “Consumer purchases in informal markets: estimates for the 1980s, prospects for the 1990s”, Journal of Retailing, Vol. 67 No. 1, pp. 22-50. |

| [55] | McDowell, J., & Novis, G. (2001). The consequences of money laundering and financial crime. Economic Perspectives, 6(2), 6-10. |

| [56] | Medina, L. & Schneider, F., (2018). Shadow economies worldwide: what did we learn over the last 20 years? International Monetary Fund working papers. African Department, Washington, DC |

| [57] | Medina, L., & Schneider, F. (2019). Shedding light on the shadow economy: A global database and the interaction with the official one. |

| [58] | Meon, P. G., & Sekkat, K. (2005). Does corruption grease or sand the wheels of growth?. Public choice, 122, 69-97. |

| [59] | Miller, M. B. (1995). Coefficient alpha: A basic introduction from the perspectives of classical test theory and structural equation modeling. |

| [60] | Ning H. (2016). Rethinking the Causes of Corruption: Perceived Corruption, Measurement Bias, and Cultural Illusion. Chinese Political Science Review 1(2): 268-302. |

| [61] | Higgins, M. (1989), Assessing the underground economy in the United Kingdom, in Feige, E. L. (ed.), The Underground Economies. |

| [62] | Neill, D. M. (1989), Growth of the underground economy 1950–81: some evidence from the current population survey, Study for the Joint Economic Committee, U.S. Congress Joint Committee Print, U.S. Gov. Printing Office, Washington, DC, pp. 98–122. |

| [63] | OECD. (2002). Measuring the Non-Observed Economy. |

| [64] | Ospina‐Velasco, J. (2003). Combating money laundering and smuggling in Colombia. Journal of Financial Crime, 10(2), 153-156. |

| [65] | Pahl, R. E. (2015). From ‘informal economy to ‘forms of work': cross-national patterns and trends. Industrial Societies (Routledge Revivals): Crisis and Division in Western Capitalism, 90. |

| [66] | Park, T. (1979), Reconciliation Between Personal Income and Taxable Income, Bureau of Economic Analysis, Washington, DC, pp. 1947–1977. |

| [67] | Pellegrini, L., & Gerlagh, R. (2004). Corruption's effect on growth and its transmission channels. Kyklos, 57(3), 429-456. |

| [68] | Peterson, H. G. (1982), Size of the public sector, economic growth, and the informal economy: development trends in the Federal Republic of Germany, Review of Income and Wealth, 28, pp. 191–215. |

| [69] | Philp M. (2015). The definition of political corruption. In P. M. Heywood (Ed.), Routledge handbook of political corruption (pp. 17–29). Abingdon, UK: Routledge. |

| [70] | Postea, M. M., & Achim, M. V. (2023). Estimation methods for the shadow economy. A systematic literature review: Métodos de estimativa para a economia subterrânea. Uma revisão sistemática da literatura. Brazilian Journal of Business, 5(3), 1574-1594. |

| [71] | Pellegata, A. (2013). Constraining political corruption: an empirical analysis of the impact of democracy. Democratization, 20(7), 1195-1218. |

| [72] | Psychoyios, D., Missiou, O., & Dergiades, T. (2021). Energy-based estimation of the shadow economy: The role of governance quality. The Quarterly Review of Economics and Finance, 80, 797-808. |

| [73] | Quiros-Romero, M. G., Alexander, M. T. F., & Ribarsky, M. J. (2021). Measuring the informal economy. International Monetary Fund. |

| [74] | Razafindrakoto M., Roubaud F. (2010). Are International Databases on Corruption Reliable? A Comparison of Expert Opinion Surveys and Household Surveys in Sub-Saharan Africa. World Development, 38(8): 1057-1069. |

| [75] | R Core Team (2017). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna. |

| [76] | Romero, V. (2022). Bloody investment: misaligned incentives, money laundering, and violence. Trends in Organized Crime, 25(1), 8-36. |

| [77] | Rigdon, E. E., Ringle, C. M., & Sarstedt, M. (2010). Structural modeling of heterogeneous data with partial least squares. Review of marketing research, 255-296. |

| [78] | Rose-Ackerman, S. (1999). Political corruption and democracy. Conn. J. Int'l L., 14, 363. |

| [79] | Sabir S, Rafque A, Abbas K (2019) Institutions and FDI: evidence from developed and developing countries. Financ Innov 5(8): 1–20. |

| [80] | Sachs, J. D., & Warner, A. M. (1997). Sources of slow growth in African economies. Journal of African Economies, 6(3), 335-376. |

| [81] | Sivona, E. U., & Riccardi, M. (2017). Assessing the risk of money laundering in Europe. Final report of project IARM. |

| [82] | Schneider, F. (2015). Size and development of the shadow economy of 31 European and 5 other OECD countries from 2003 to 2014: different developments? Journal of Self-Governance and Management Economics, 3(4), 7-29. |

| [83] | Schneider, F. (2019). Size of the shadow economies of 28 European Union countries from 2003 to 2018. In European Union (pp. 111-121). |

| [84] | Schneider, F., & Enste, D. H. (2000). Shadow economies: Size, causes, and consequences. Journal of Economic Literature, 38(1), 77-114. |

| [85] | Schneider, F., Buehn, A., & Montenegro, C. E. (2010). New estimates for shadow economies all over the world. Int. Econ. J. 24(4), 443–461. |

| [86] | Schneider, F., Raczkowski K., Mróz, B., (2015), "Shadow economy and tax evasion in the EU," Journal of Money Laundering Control, Vol. 181 pp. 34-51. |

| [87] | Seligson M. A. (2006). The measurement and impact of corruption victimization: survey evidence from Latin America. World Development, 34(2): 381–404. |

| [88] | Serra, D. (2006). Empirical determinants of corruption: A sensitivity analysis. Public Choice, 126(1-2), 225-256. |

| [89] | Schuberth, F., Rademaker, M. E., & Henseler, J. (2023). Assessing the overall fit of composite models estimated by partial least squares path modeling. European Journal of Marketing, 57(6), 1678-1702. |

| [90] | Slama, M. B., & Gueddari, A. (2022). The relationship between money laundering and economic growth in the MENA region—a simultaneous equation model. In Key Challenges and Policy Reforms in the MENA Region: An Economic Perspective (pp. 123-141). Cham: Springer International Publishing. |

| [91] | Smith, P. (1994), Assessing the size of the underground economy: the Canadian statistical perspectives, Canadian Economic Observer, 11, pp. 16–33. |

| [92] | Stancu, I., & Rece, D. (2009). The Relationship between Economic Growth and Money Laundering--a Linear Regression Model. Theoretical & Applied Economics, 16(9). |

| [93] | Standaert, S. (2015). Divining the level of corruption: a Bayesian state-space approach. Journal of Comparative Economics, 43(3), 782-803. |

| [94] | Svensson, J. (2005). Eight questions about corruption. Journal of economic perspectives, 19(3), 19-42. |

| [95] | Tanzi, V. (1980), The underground economy in the United States: estimates and implications, Banca Nazionale del Lavoro, 135, pp. 427–453. |

| [96] | Tanzi, V. (1983), The underground economy in the United States: annual estimates, 1930–1980, IMF Staff Papers, 30, pp. 283–305. |

| [97] | Tanzi, V. (1998). Corruption around the world: Causes, consequences, scope, and cures. Staff papers, 45(4), 559-594. |

| [98] | Tanzi, V. 1997. “Macroeconomic Implications of Money Laundering,” in Responding to Money Laundering, International Perspectives, 91-104. Amsterdam: Harwood Academic Publishers. |

| [99] | The IMF and the Fight against money laundering and terrorism. (2023). Triesman, D. (2000). The causes of corruption: a cross-national study. Journal of Public Economics, 76(3), 399-457. |

| [100] | Uberti, L. J. (2022). Corruption and growth: Historical evidence, 1790–2010. Journal of Comparative Economics, 50(2), 321-349. |

| [101] | Lambsdorff, J. G. (1999). The Transparency International corruption perceptions index 1999: Framework document. Transparency International, Berlin. |

| [102] | Unger B (2007). Black Finance. The Economics of Money Laundering. Cheltenham, UK: Edward Elgar. |

| [103] | Unger B, Siegel M, Ferwerda J, de Kruijf W, Busuioic M, Wokke K, Rawlings G (2006) The amounts and the effects of money laundering. Report for the Ministry of Finance, 16. Utrecht School of Economics, Netherlands. |

| [104] | Usakli, A., & Rasoolimanesh, S. M. (2023). Which SEM to use and what to report? A comparison of CB-SEM and PLS-SEM. In Cutting edge research methods in hospitality and tourism (pp. 5-28). Emerald Publishing Limited. |

| [105] | Walker J (1995). Estimates of the Extent of Money Laundering in and through Australia. Paper prepared for Australian Transaction Reports and Analysis Centre (ATRAC), September by John Walker Consulting Services. |

| [106] | Walker J (1999). “How Big is Global Money Laundering?” 3(1) Journal of Money Laundering Control 25-37. |

| [107] | Walker J (2002). “Just How Big is Global Money Laundering?”, a seminar presented at the Australian Institute of Criminology, Sydney. |

| [108] | Walker J (2003a). The Profits & Losses of Global Crime. Ontario: de Sitter Publications. |

| [109] | Walker J (2003b). “The Global Response to Money Laundering,” Lecture in Bangkok, Thailand. |

| [110] | Warde, I. (2007). The war on terror, crime, and the shadow economy in the MENA countries. Mediterranean Politics, 12(2), 233-248. |

| [111] | Williams, C., & Windebank, J. (2001). Reconceptualizing paid informal exchange: some lessons from English cities. Environment and Planning A, 33(1), 121-140. |

| [112] | Williams, L. J., Edwards, J. R., & Vandenberg, R. J. (2003). Recent advances in causal modeling methods for organizational and management research. Journal of Management, 29(6), 903-936. |

| [113] | Wold, H.: Soft modeling: The basic design and some extensions. In: Joreskog, K. G., Wold, H. (eds.) Systems Under Indirect Observations, Part II, Chapter I, pp. 1–54. North Holland, Amsterdam (1982). |

| [114] | World Bank. (1997a). Helping countries combat corruption: The role of the World Bank. Washington D.C. |

| [115] | Yoo, T., & Hyun, J. K. (1998). International comparison of the black economy: Empirical evidence using micro-level data. Paper Presented at 1998 Congress of Int. Institute Public Finance. |

| [116] | Zhao, X., Lynch Jr, J. G., & Chen, Q. (2010). Reconsidering Baron and Kenny: Myths and truths about mediation analysis. Journal of Consumer Research, 37(2), 197-206. |

APA Style

Ahmad, R., Nauman, M. (2026). Shadows of Influence: Money Laundering, Corruption, Black Market and Socio-economic Development Worldwide: A PLS-SEM Analysis. Research & Development, 7(1), 1-23. https://doi.org/10.11648/j.rd.20260701.11

ACS Style

Ahmad, R.; Nauman, M. Shadows of Influence: Money Laundering, Corruption, Black Market and Socio-economic Development Worldwide: A PLS-SEM Analysis. Res. Dev. 2026, 7(1), 1-23. doi: 10.11648/j.rd.20260701.11

@article{10.11648/j.rd.20260701.11,

author = {Rizwan Ahmad and Muhammad Nauman},

title = {Shadows of Influence: Money Laundering, Corruption, Black Market and Socio-economic Development Worldwide: A PLS-SEM Analysis},

journal = {Research & Development},

volume = {7},

number = {1},

pages = {1-23},

doi = {10.11648/j.rd.20260701.11},

url = {https://doi.org/10.11648/j.rd.20260701.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.rd.20260701.11},

abstract = {The intricacies surrounding the measurement and modelling of money laundering (ML), corruption (COR), and black-market prevalence (BMP), as well as their effects on socio-economic development (SD), introduce significant challenges to accurately capturing and understanding these phenomena. There is a plethora of theories on individual measurements of each concept, but regrettably, they are not immune to criticism, and no such explicit approach is available to study the nexus between these complex concepts. The current study employs the multiple indicator approach to measure ML, COR, and SD, and utilizes the PLS-SEM approach to explore the relationships between these complex concepts, with a focus on the mediating role of the BMP. The per capita investment (PCI) expenditures, modelled through the multiple indicator approach, have been used as the control variables. The study has adopted a data-driven approach to conduct pre- and post-estimation analysis for the constructs and validate the results for a cross-section of 198 countries in 2022. The results indicate that the impact of corruption on socio-economic development is negative and statistically significant. The black market has a direct, negative, and significant impact on socio-economic development; similarly, the BMP has a positive and significant effect on ML. In addition to the direct impact on socio-economic development, BMP also indirectly affects SED through the ML. The direct effects of ML on SED are adverse, while it has an indirect positive impact on SED through its significant multiplier effect on per capita investment. These findings have implications for anti-money laundering and anti-corruption policies worldwide.},

year = {2026}

}

TY - JOUR T1 - Shadows of Influence: Money Laundering, Corruption, Black Market and Socio-economic Development Worldwide: A PLS-SEM Analysis AU - Rizwan Ahmad AU - Muhammad Nauman Y1 - 2026/03/09 PY - 2026 N1 - https://doi.org/10.11648/j.rd.20260701.11 DO - 10.11648/j.rd.20260701.11 T2 - Research & Development JF - Research & Development JO - Research & Development SP - 1 EP - 23 PB - Science Publishing Group SN - 2994-7057 UR - https://doi.org/10.11648/j.rd.20260701.11 AB - The intricacies surrounding the measurement and modelling of money laundering (ML), corruption (COR), and black-market prevalence (BMP), as well as their effects on socio-economic development (SD), introduce significant challenges to accurately capturing and understanding these phenomena. There is a plethora of theories on individual measurements of each concept, but regrettably, they are not immune to criticism, and no such explicit approach is available to study the nexus between these complex concepts. The current study employs the multiple indicator approach to measure ML, COR, and SD, and utilizes the PLS-SEM approach to explore the relationships between these complex concepts, with a focus on the mediating role of the BMP. The per capita investment (PCI) expenditures, modelled through the multiple indicator approach, have been used as the control variables. The study has adopted a data-driven approach to conduct pre- and post-estimation analysis for the constructs and validate the results for a cross-section of 198 countries in 2022. The results indicate that the impact of corruption on socio-economic development is negative and statistically significant. The black market has a direct, negative, and significant impact on socio-economic development; similarly, the BMP has a positive and significant effect on ML. In addition to the direct impact on socio-economic development, BMP also indirectly affects SED through the ML. The direct effects of ML on SED are adverse, while it has an indirect positive impact on SED through its significant multiplier effect on per capita investment. These findings have implications for anti-money laundering and anti-corruption policies worldwide. VL - 7 IS - 1 ER -

Pakistan Institute of Development Economics, Islamabad, Pakistan

N.C.B.A&E, Lahore, Pakistan

Information